UK savings market trends 2024

This page includes relevant UK savings market trends for 2024, such as average savings, average UK wealth statistics, plus student savings trends and the state of UK pensions.

As part of our study into recent UK savings market trends, we conducted an extensive examination of the state of UK savings in 2024, including differences between genders and age groups.

We also took a deep dive into how students are coping with the ongoing cost-of-living crisis and the resultant squeeze on their savings, as well as how well the triple pension lock has affected savings among the older generation. Our findings make for fascinating reading.Ìý

Top 10 UK savings market trends

ÌýLondoners saved an average of £269.07 per month in 2022, making them the UK’s highest monthly savers.ÌýÌýÌýÌýÌý

ÌýUK men aged 65 and over have average savings totalling almost £130,000 more than women in the same age group.

Workers in public administration and defence had the highest individual wealth in 2020, with a forecasted average individual wealth for 2024 of over £390,000.ÌýÌýÌýÌýÌý

During the second quarter of 2023, the average UK household saved 9.1% of their income.ÌýÌýÌýÌýÌý

The average UK household’s saving ratio spiked to 26.8% in the second quarter of 2020 as a result of the Covid-19 lockdown.

Between 2011/12 and 2021/22, average disposable income in the UK rose by more than 11%, from £35,421 to £39,328.ÌýÌýÌýÌýÌý

In 2020, people aged 60-64 had the highest average wealth by age in the UK, with a median wealth of £381,100.ÌýÌýÌýÌýÌý

Approximately seven in 10 (71%) students surveyed in 2023 had considered dropping out of university, with 54% citing financial worries as t

he reason.ÌýÌýÌýÌýÌý

On average, UK students’ maintenance loans fall short of their living costs by £582 per month compared to £439 in 2022.ÌýÌýÌýÌýÌý

In October 2023, the rate of UK inflation stood at 4.7%.ÌýÌýÌýÌýÌý

UK savings market trend statisticsÌý

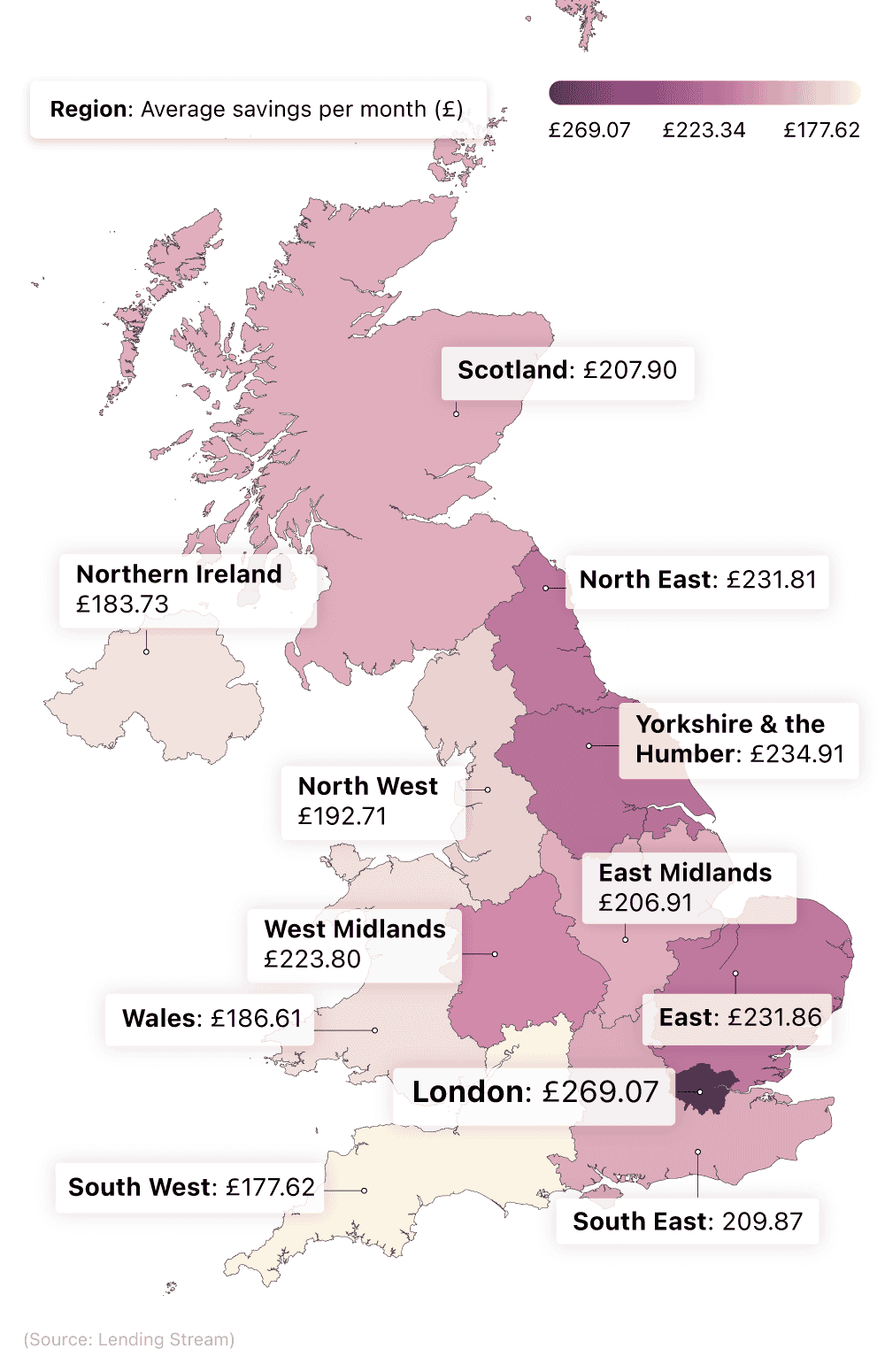

Which region has the highest annual savings?

UK savings statistics for 2024 highlight that London residents have the highest monthly savings of anyone in the UK, when looking at the average savings rate by UK region. With average monthly savings of almost £270 per month (£3,240 per year), this figure suggests that the typically higher wages in the capital have had an impact on total savings.

Less than £3 per month separated second place (Yorkshire and Humber) and fourth place (North East) in the study, suggesting that similar savings habits can be found in much of the UK.Ìý

A breakdown of average annual savings in the UK by region

Of all the English regions, only the North West and South West recorded average savings figures of below £200 per month, with the South West’s total of £177.62 the lowest in the study. Northern Ireland and Wales recorded the next lowest average savings across the UK, with monthly totals of £183.73 and £186.61, respectively.Ìý

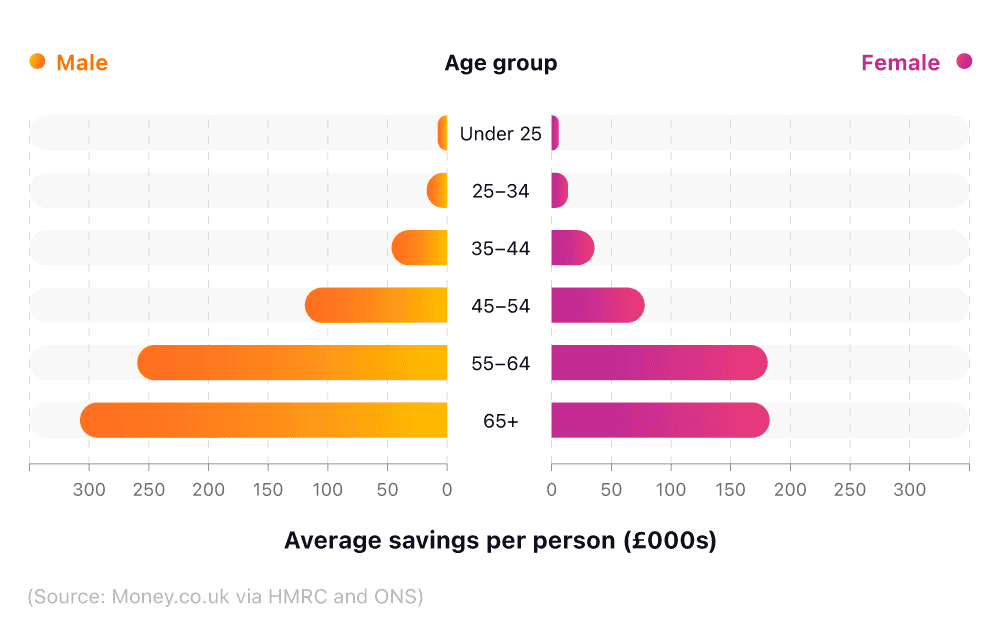

Average UK savings by gender and age

As part of our research for UK savings market trends in 2022, we looked at the average savings of men and women across six age groups. The data combined the mean ISA savings and pension savings of each age group to provide one combined figure for average UK savings by age and gender.

In every age bracket, there was a considerable gap in the average UK savings by gender between men and women, with men acquiring considerably more every time. The substantial savings gap begins early, with a male average of £7,756 for those aged 25 and below being 25% higher than females in the same age group.

This financial gulf only accelerates as men continue to accumulate more savings over time. The gap becomes increasingly pronoun

ced by age 45-54, where the average male has acquired almost 35% more savings than women of the same age.

A breakdown of average UK savings by age group and gender (exclusive data)

In monetary terms, the savings disparity peaks in our oldest age group, with men aged 65+ having average savings of almost £130,000 more than women of the same age.Ìý

Though men had greater ISA savings in every age category, it was in pensions that the biggest gulf in savings between the genders could be seen. By age 65+, the average man will have acquired pension savings of £260,500, with the average woman acquiring £137,400 (around 50% less than her average male counterpart).

These figures indicate that, while men save

more on average, the extent of the difference may be largely due to higher average salaries for men and thus increased pension contributions for men in the workplace.Ìý

UK average savings by industry (exclusive data)

Our data on the average savings by industry in the UK found those who worked in public administration and defence to have the highest individual wealth. Workers in this industry had an average individual wealth of £289,500 between April 2016 and March 2018, with that number forecasted to rise by more than 30% by April 2022 and March 2024.

Real estate and mining and quarrying were the other two industries in our study expected to have an average individual wealth of more than £300,000 by 2024. While real estate came second to public administration and defence for individual wealth, the industry’s projected financial wealth increase of £8,356 was more than double the numbers of any other industry.Ìý

A breakdown of UK average savings by industry

| Individual wealth (£) | Forecasts | ||||

|---|---|---|---|---|---|

| Industry | April 2014 - March 2016 | April 2016 - March 2018 | April 2018 - March 2020 | April 2020 - March 2022 | April 2022 - March 2024 |

| Accommodation and food service | 22,400 | 21,500 | 26,100 | 27,033 | 28,883 |

| Administrative and support service | 47,200 | 53,600 | 55,500 | 60,400 | 64,550 |

| Arts, entertainment and recreation | 77,500 | 82,900 | 75,100 | 76,100 | 74,900 |

| Construction | 105,300 | 115,000 | 115,500 | 122,133 | 127,233 |

| Education | 212,900 | 213,700 | 237,400 | 245,833 | 258,083 |

| Electricity, gas, steam and air conditioning | 219,600 | 235,900 | 249,800 | 265,300 | 280,400 |

| Financial and insurance | 225,000 | 266,300 | 267,900 | 295,967 | 317,417 |

| Human health and social work | 123,500 | 149,900 | 151,600 | 169,767 | 183,817 |

| Information and communication | 185,900 | 213,000 | 230,900 | 254,933 | 277,433 |

| Manufacturing | 123,300 | 143,100 | 140,800 | 153,233 | 161,983 |

| Mining and quarrying | 212,500 | 215,000 | 269,300 | 289,067 | 317,467 |

| Other service activities | 104,000 | 127,300 | 126,700 | 142,033 | 153,383 |

| Professional, scientific and technical | 206,000 | 223,800 | 243,700 | 262,200 | 281,050 |

| Public administration and defence | 258,600 | 289,500 | 325,200 | 357,700 | 391,000 |

| Real estate | 159,100 | 182,500 | 267,500 | 311,433 | 365,633 |

| Transportation and storage | 110,600 | 130,300 | 123,200 | 133,967 | 140,267 |

| Water supply, sewerage and waste management | 75,600 | 89,300 | 89,800 | 99,100 | 106,200 |

| Wholesale and retail trade, repair of motor vehicles and motorcycles | 59,400 | 68,800 | 78,900 | 88,533 | 98,283 |

(Source: money.co.uk via ONS)

At the other end of the table was the accommodation and food service industry. This industry was the only one to show a decrease in individual wealth between April 2014-March 2016 and April 2016-March 2018. With a projected increase of nearly £29,000 between April 2022-March 2024, accommodation and food services recorded a projected individual wealth that was less than half the total of the next lowest industry (administrative and support services).Ìý

This sector, along with arts and recreation, were the two industries with the lowest average wealth in the UK, with recorded wealth forecasts for April 2022-March 2024 of £65,550 and £74,900, respectively.Ìý

Average UK household savings

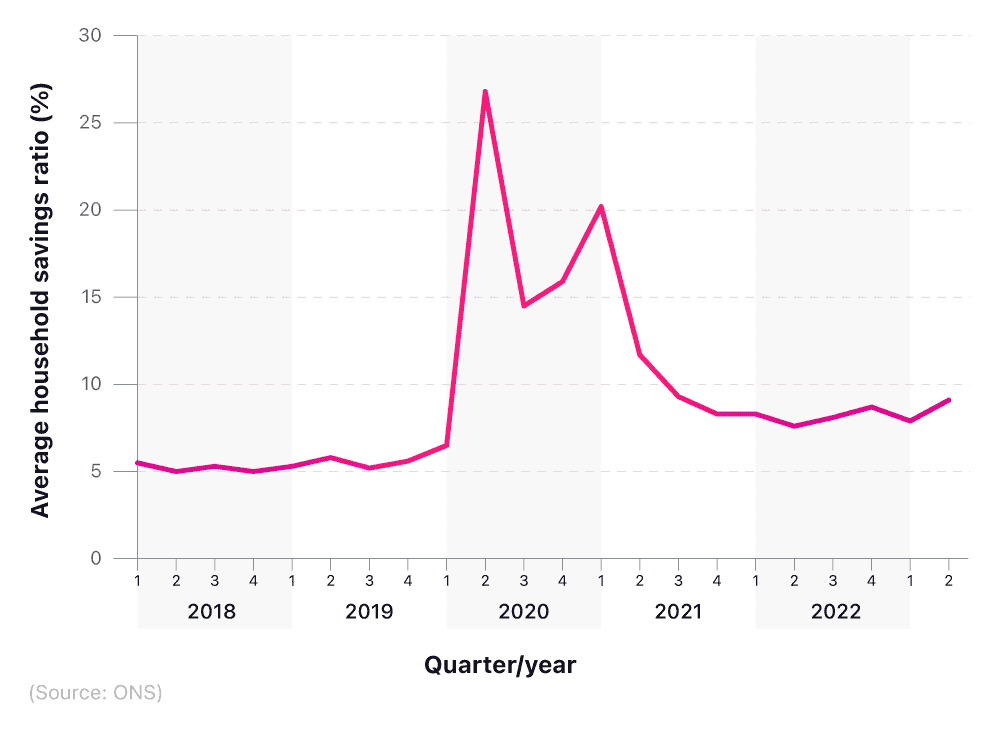

Savings facts from the Office of National Statistics (ONS) show that the average UK household saved 9.1% of its income in the second quarter of 2023.Ìý

The figures for the average UK household savings ratio reflect the unpredictable nature of the economy, wages, and the cost of living over the last decade. After a high point of 10.4% in Q3 2015, the savings ratio began to fall steadily over the following few years.

The peak of the slump occurred in Q1 2017 when the household savings ratio sunk to 3.3%. While this figure came as part of a wider downward trend, the particularly low percentage may be down to the economic and social unrest following the Brexit referendum the previous summer.

A breakdown of average UK household savings by quarter between 2013 and 2022

While the ratio would increase from this point and settle at between 5% and 6% in subsequent years, it remained some distance away from the UK household savings statistics recorded pre-2016. This would change dramatically in Q2 2020, however, when the ratio soared to 26.8% in the wake of the Covid-19 pandemic.

The household savings stats remained unusually high throughout the pandemic, with rises and falls in line with increases and decreases in lockdown restrictions. While the year to date has seen the savings ratio settle, the first and second quarter figures of 7.9% and 9.1% suggests that people are still concerned about the economic situation, and are keen to save more of their income than they once did.

Average UK wealth statisticsÌý

UK average household wealth

Annual data on average household wealth in the UK shows a slow rise in household disposable income over the last decade, despite a backdrop of economic turmoil. Between 2011/12 and 2021/22, the average disposable household income in the UK has risen by 11%, from £35,421 to £39,328.

A breakdown of UK average household disposable income by year

| Year | Average equivalised disposable income by household |

|---|---|

| 2011/12 | £35,421 |

| 2012/13 | £34,735 |

| 2013/14 | £36,153 |

| 2014/15 | £36,875 |

| 2015/16 | £38,078 |

| 2016/17 | £37,596 |

| 2017/18 | £37,330 |

| 2018/19 | £37,724 |

| 2019/20 | £39,218 |

| 2020/21 | £38,994 |

| 2021/22 | £39,328 |

(Source: ONS)

While this rise represents a substantial increase over the last decade, there have been two instances where disposable income has decreased from one year to the next. First between 2011/12 and 2012/13 when it fell by 1.9% and again between 2015/16 and 2016/17 when it dropped by 1.3%.

The biggest monetary increase occurred between 2014/15 and 2015/16, when household disposable income increased by nearly £1,500, from £36,875 to £38,078.

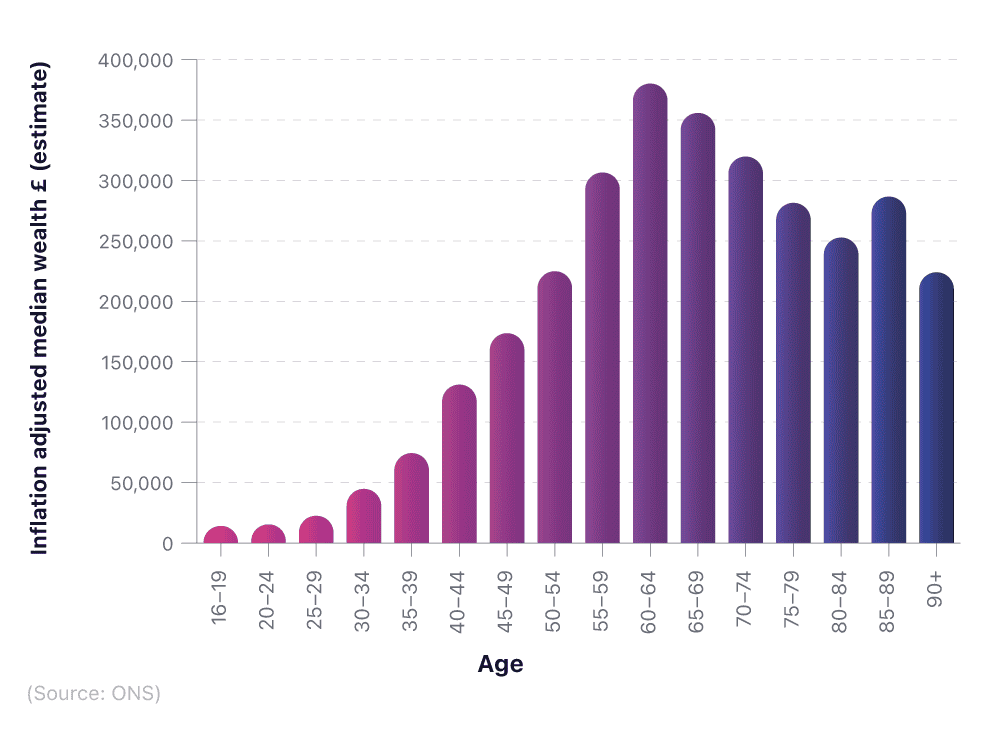

UK average wealth by age

With a median wealth of £381,100, people aged between 60-64 have the highest average wealth by age in the UK as of March 2020. The data shows that average wealth rises in every age group from 16 to 64, with the numbers reducing from 65-69 onwards.Ìý

A breakdown of inflation-adjusted median wealth across different age groups in the UK

The biggest percentage increase can be found between the age groups 25-29 and 30-34, where the median wealth almost doubles from £22,400 to £44,700.Ìý

The biggest monetary increase can be found between the age groups 55-54 and 55-59, when average wealth accelerated by over £80,000.

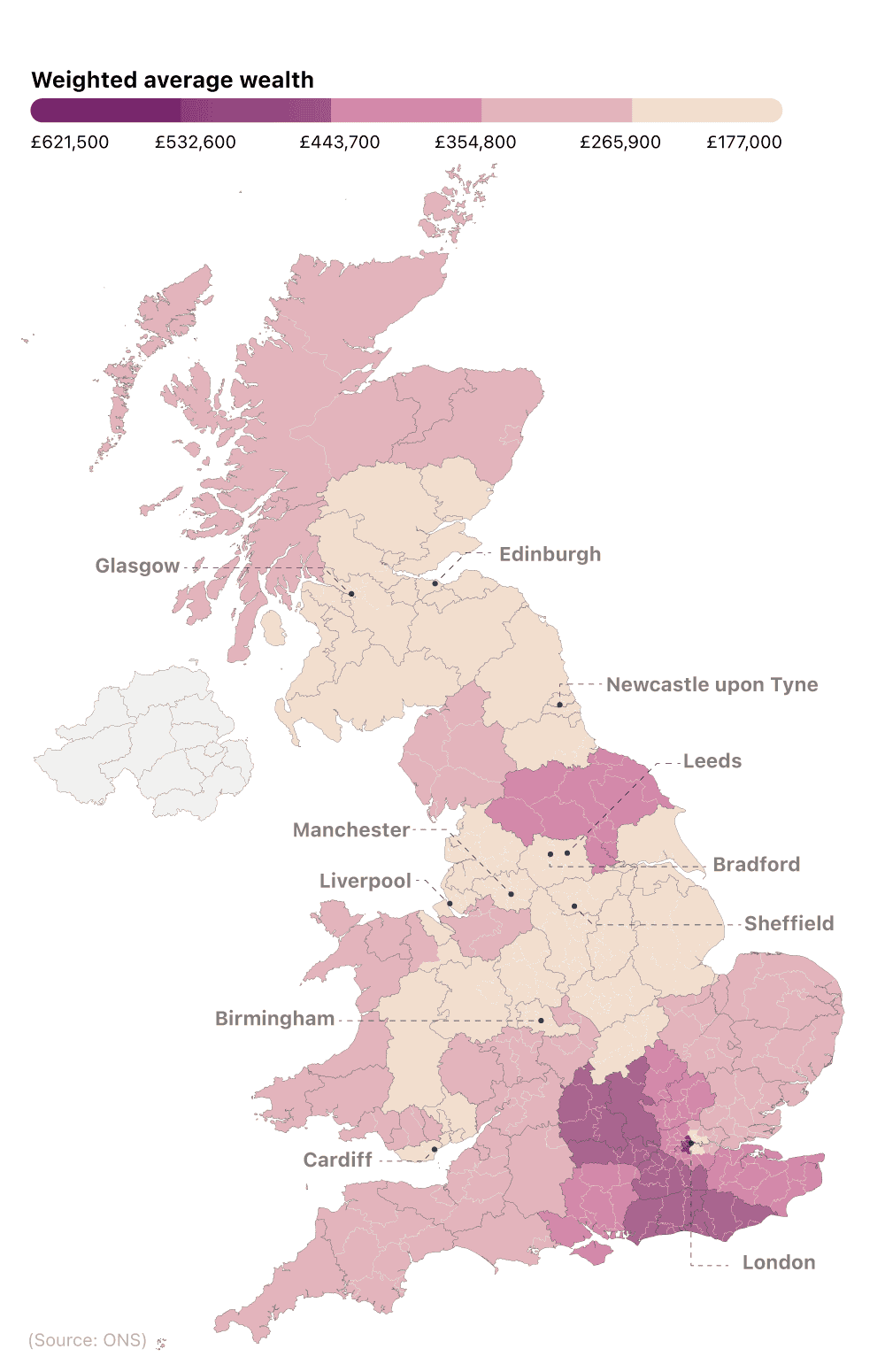

UK average wealth by region

According to regional UK savings market trends, Inner London-West is the region with the highest annual wealth across Great Britain as of March 2020. With an estimated wealth of £621,000, the capital’s figures were more than £120,000 higher than Surrey, East and West Sussex—the place with the second-highest figures in the average wealth by regional statistics.Ìý

The figures show a significant difference in average wealth by region between northern and southern areas of England, with southern regions responsible for each of the top five places and every average wealth above £400,000.Ìý

A breakdown of weighted average UK wealth by region

Of the northern regions, North Yorkshire’s average wealth of £398,200 was the highest in the study, with North Eastern Scotland’s total of £334,800 the highest average wealth in Scotland.

At the other end of the table, bottom-placed East Yorkshire and Lincolnshire’s average wealth of £177,000 was more than 70% less than Inner London-West, highlighting the significant differences in capital wealth across Great Britain. The only other region to record an average wealth below £200,000 was the West Midlands with figures of £196,500.

UK student savings statistics 2024

According to student savings stats from the 2023 Student Money Survey, more than seven in 10 (71%) students surveyed admitted they had considered dropping out of university, with 54% citing financial worries as the reason. By comparison, just over half (52%) of all students surveyed in 2022 thought about leaving university because of money worries. This was a significant increase over 2021 when around two in five (41%) students considered quitting.Ìý

The 2023 report also indicated that over a third (35%) of students claimed to use their overdraft as a source of income, with 42% saying they turn to their bank and 43% to their savings, in the case of a cash emergency.Ìý

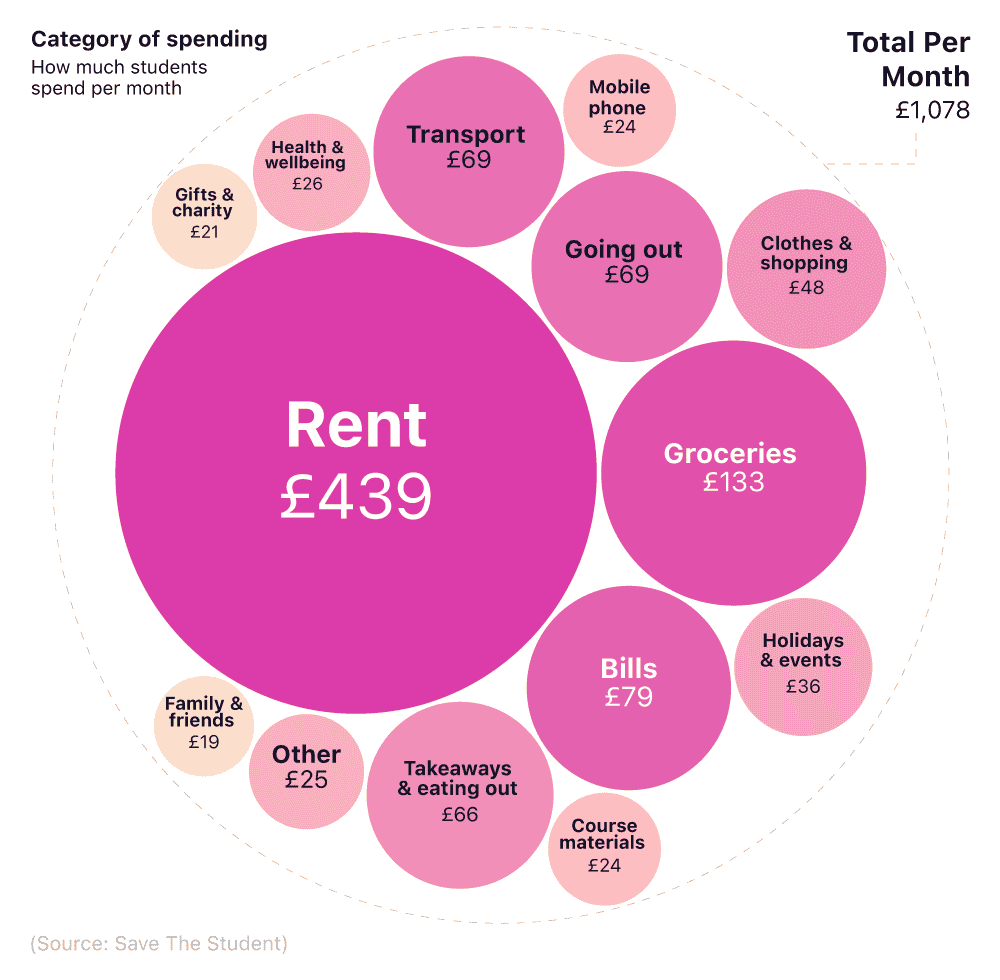

A breakdown of average UK student monthly spendingÌýÌýÌýÌýÌýÌý

(Source: Save the Student)

According to recent student savings statistics, the average student spent £1,078 per month on outgoings in 2023 – a 17% increase on the previous year.Ìý

Rent accounts for 41% of a student’s monthly living costs, followed by groceries (12%), and energy bills (7%).Ìý

The average maintenance loan for a UK student is £496 per month. In real terms, this covers less than half (46%) of a typical student’s monthly outgoings, resulting in a shortfall of £582 per month. In the 2022 survey, the corresponding figure for the shortfall was £439 per month, whilst, in 2021, it was £340, highlighting the fact that students in 2023 are almost £250 a month worse off compared to those in 2021.

In 2023/24, the maximum funding for UK students’ living costs will increase by:

40% for Northern Irish students.Ìý

Between 11.7% to 17.6% for Scottish students.

9.4% for Welsh students.Ìý

2.8% for English students.

These figures, while welcomed by the UK student population, are likely to be dwarfed by the rising cost of living and inflation.Ìý

As of October 2023, the rate of UK inflation stood at 4.7%, with food price inflation 10.1%. These figures are considerably above the Bank of England’s 2% target for the rate of inflation, yet at the same time in 2022, things were much worse, with inflation hitting a 41-year high of 11.1%. This means their already-stretched maintenance loans will need to go further, and UK students either face cuts in their expenditure or increases in their level of income.Ìý

Some students may turn to the ‘Bank of Mum and Dad’ to help them out financially while at university. Even so, the average UK student receives £227 a month from their parents, up from £149.80 in 2022.Ìý

As a result, when surveyed in 2023, almost two-thirds (64%) of UK students felt the maintenance loan wasn’t enough for them to live on. Just under half (46%) used their savings as a source of money – down from 57% in 2022 and 50% in 2021.Ìý

Savings was the fourth most common response given when asked about their sources of money. Ahead of it came:

Part-time jobs (56%)

Parents (53%)

Maintenance loans (52%)

Other sources included overdraft (35%) and grants and funding (26%).Ìý

According to the 2023 Student Money Survey, almost two-thirds (64%) of students don’t expect to ever be able to repay their loans in full. Many students don’t fully understand the loans they have taken out, with 62% admitting that they didn’t know their loan’s interest rate, whilst a further 42% don’t understand their loan agreement.

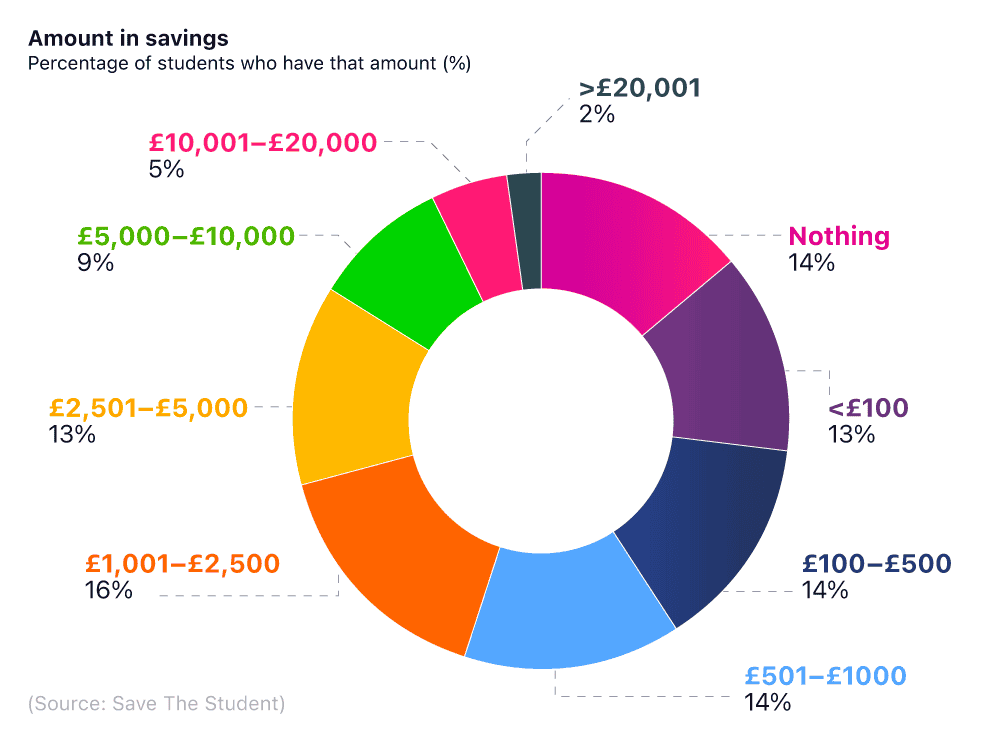

A breakdown of average savings in UK student savings accountsÌý

The average amount of money that UK students had in their savings in 2023 was £2,650,Ìý which surprisingly is over twice as much as last year’s average of £1,280.ÌýÌý

Sixteen percent of respondents claimed to have between £1,001 and £2,500. This was the most popular response, narrowly beating the no savings category (14%), which was the joint-second most popular response, alongside £101 to £500 and £501 to £1,000.Ìý

In all, more than a quarter (27%) of students had less than £100 in their savings.Ìý

Just 2% of students had more than £20,000 in their bank account, while 5% had between £10,001 and £20,000.Ìý

Student ISA accounts

Lifetime ISAs (LISAs) can help you save up to £4,000 a year. Every financial year (April to April), the Government pays a 25% bonus on the amount saved, meaning you could receive up to £1,000 each year for no cost. This bonus only applies, however, if you use the savings to buy your first house or after you turn 60.Ìý

A survey by Save The Student found that almost a third (32%) of students questioned didn’t know what a LISA was. Just under a fifth (18%) had one, while the remaining 50% were aware of them but hadn’t opened one.

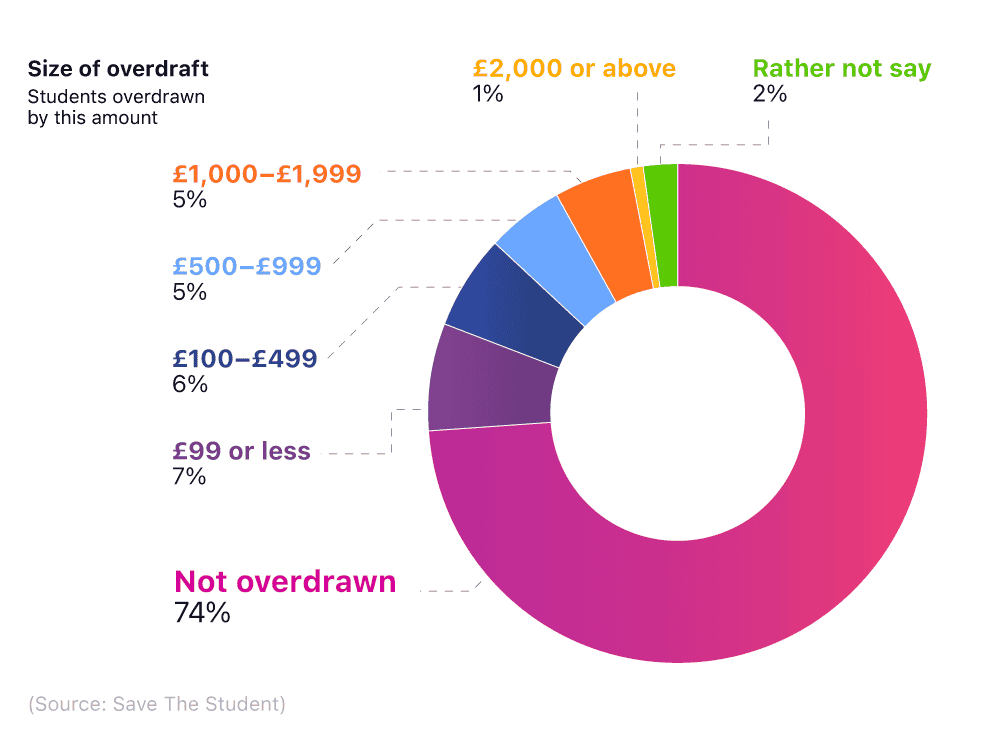

A breakdown of the size of UK student overdrafts and the percentage of students who are overdrawn by this amountÌý

Around three-quarters (74%) of students surveyed admitted to not being overdrawn at all, with 13% going into their overdraft by up to £500.Ìý

Amongst students who have overdrafts, just over a quarter (27%) had hit their overdraft limit at some point in the past, with almost half (46%) not knowing when to repay their overdraft.Ìý

More than one in five (22%) of students said they have used buy now, pay later (BNPL) sites, such as Klarna, Clearpay, and PayPal Credit, with 5% stating they used these sites regularly.Ìý

Factors affecting savings in the UK 2024

UK interest rates statisticsÌý

The best place to save your money is more complex than just picking the savings account with the highest rate of interest. Despite this, the rate of interest you get on your money will likely be a deciding factor.Ìý

In November 2022, the Bank of England (BoE) increased the benchmark base rate from 2.25% to 3%—the eighth consecutive hike since December 2021, and the highest for 14 years. This also happened to be the biggest single increase in the base rate since 1989.Ìý

This followed a 0.5 percentage point increase in September 2022 (1.75% to 2.25%). Since then, the BoE has made several subsequent increases to the base rate, which reached 4% on February 2, 2023. By August 2023, the rate had hit 5.25%, a percentage that has remained unchanged as of November 2023.Ìý

With high interest rates, some may question: is having a savings account worth it? The good news for savers in 2023 is that with rising interest rates, banks and building societies normally pass these on to the consumer. This provides competitive deals, encouraging people to save with them and help get a decent return on your savings.Ìý

As of October 2023, the Annual Equivalent Rate (AER) for an instant-access savings account was 5.25%, whereas for a cash ISA account, the corresponding figure was 5.65%. In the same month, rates on easy-access savings accounts reached 5.25%, and for those willing to lock their savings in for a year in a fixed-rate cash ISA, or a fixed-rate bonds account, returns were 5.8%.Ìý

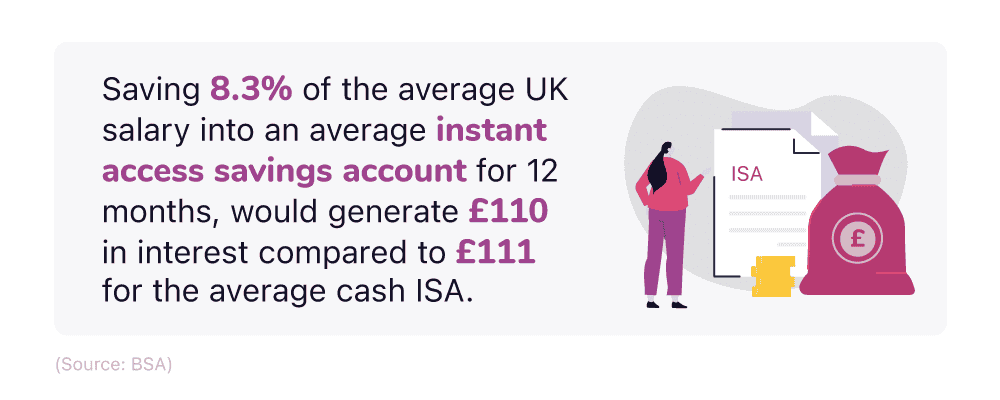

The main benefit of an ISA is that you can earn interest tax-free. If someone with an average salary (around £32,000 a year) saved 8.3% of their after-tax income into an average instant-access savings account paying 5.16% for 12 months, they would receive £110.42 in interest (after tax). Compared to the average cash ISA (paying 5.2%) where this figure would be nearer £111.28.

In a 2023 survey by the Building Societies Association, over a third (34%) of people surveyed admitted they never checked what interest rate they were getting with their bank or building society.Ìý

If you’re looking to play the long game, you may wish to choose a lifetime ISA, earning you 25% on savings up to £4,000 a year. Or you may like to choose a fixed-bond savings account, that ties your money up for a set term, during which you agree not to make a withdrawal. A savings bond normally requires that you invest a set sum of money (usually a minimum of £100, but sometimes up to £5,000) in return for a fixed rate of interest over a set period.Ìý

Alternatively, if you’re after a more flexible savings account, you may opt for a notice savings account, which has common notice periods ranging from seven to 30 days, extending up to 120 days.

Studies have also found that hoarding cash at home can be bad for your financial health, therefore the best place for your money is in a savings account. Savers can now get over 2% on a savings account, while still maintaining access to their money.Ìý

UK savings market trends highlight that throughout 12 months, savers could be missing out on around £565 per year on a £10,000 savings pot purely by choosing not to switch to a savings account with a rate of interest around the 5.65% mark.Ìý

In 2023, the effective interest rate paid on new fixed-term savings accounts rose from 4.58% in July 2023 to 4.75% in August 2023. This is a staggering rise compared to the same period last year, when the effective interest was 1.27% in July and 1.55% in August. In July 2021, the respective figure stood at just 0.07%.Ìý

Household savings since the cost of living crisisÌý

The question of how to save money during the cost of living crisis will be an anxious topic for many across the UK.Ìý

According to recent cost of living statistics, a third of savers (33%) admitted if they lost their income, they wouldn’t have enough in their savings to cover living costs for the following month.Ìý

More than a third (36%) of UK savers surveyed between September and October 2022 said they were relying on their savings to get them through the cost of living crisis. More than half (55%) have reduced their savings contributions, with over a third (35%) not saving anything during this financially difficult time.Ìý

Triple pension lockÌý

Under the UK’s current triple pension lock, the State Pension is due to increase each year in line with inflation, average increase in UK wages, or 2.5% (whichever is the highest).Ìý

A breakdown of how the triple pension lock is calculated

| Financial year | Factor | Based on: | Consumer Price Index (CPI) inflation | Average earnings | Retail Price Index (RPI) inflation |

|---|---|---|---|---|---|

| 2019/20 | 0.026 | Earnings | 0.024 | 0.026 | 0.033 |

| 2020/21 | 0.039 | Earnings | 0.017 | 0.039 | 0.024 |

| 2021/22 | 0.025 | 2.50% | 0.005 | -1.00% | 0.011 |

(Source: House of Commons Library)

The triple pension lock was introduced in 2010 by the Conservative/Liberal Democrat coalition government, and comes into effect each April.Ìý

The triple lock pension aims to ensure the value of the state pension keeps pace with the cost of living. It does this by increasing state pensions each year by the earnings growth rate, inflation rate or 2.5% (whichever is the highest). It protects only the full, basic State Pension of £156.20 per week and the full, new State Pension of £203.85.Ìý

As the triple pension lock index rises each year by the highest of the three indicated factors, it becomes more generous than each of the individual components, which compounds over time.Ìý

A breakdown of how the price of the triple pension lock would vary by each financial year

| Financial year | Actual value of State Pension (triple-locked) | State Pension (if it were based on Consumer Price Index (CPI)) | State Pension (if it were based on average earnings) | State Pension (if it were based on the higher of CPI or earnings) |

|---|---|---|---|---|

| 2019/20 | £129.20 | £121.55 | £120.05 | £127.00 |

| 2020/21 | £134.25 | £123.60 | £124.75 | £132.05 |

| 2021/22 | £137.60 | £124.20 | £123.60 | £132.70 |

| 2022/23 | £141.85 | £128.00 | £134.00 | £136.85 |

| 2023/24 | £156.20 | £140.90 | £141.20 | £150.65 |

(Source: House of Commons Library)

The full basic State Pension for an individual in 2023/24 will be £156.20 per week, which is:Ìý

10.9% higher than if it had been CPI-indexed since 2011/12.

10.6% higher than if it had been linked to average earnings since 2011/12.

3.7% higher than if it had been ‘double-locked’ in line with earnings or CPI, without the 2.5% minimum increase.Ìý

Before the Autumn mini-budget of 2022, the UK Government was planning to increase state benefits in line with average wages, resulting in a rise of 5.7% and savings of £6 billion in 2023.Ìý

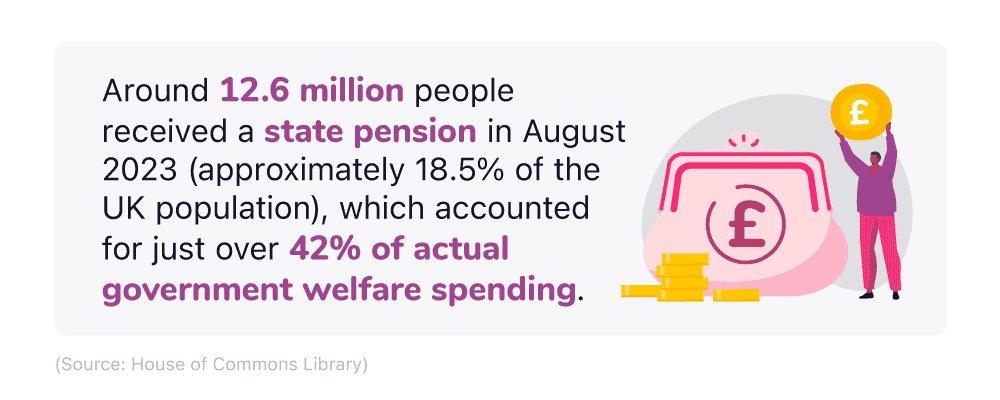

Around 12.6 million people received a state pension in August 2023 (approximately 18.5% of the UK population).Ìý

In 2023/24, this equated to approximately £124.3 billion worth of spending—a £19.4 billion increase from 2021-22.

The Department for Work and Pension (DWP) forecast that total State Pension expenditure would be:

£9.8 billion (7.9%) less than if the triple-lock had been upgraded in line with average earnings since 2011/12.Ìý

£10 billion (8%) less than if the triple lock expenditure had instead been increased in line with the CPI since 2011/12.

£3.6 billion (2.9%) less than if triple-locked expenditure had been double-locked.

Those who have no other source of income above retirement age, can also claim for pension credit, which increased by 10.1% in April 2023. Back in August 2021, 1.4 million people received pension credit – although this doesn’t include those who are eligible and didn’t claim it.Ìý

Regardless of the financial pressures caused by rising living costs, almost two-thirds (64%) of those with no savings claimed they could probably save at least £10 a month.Ìý

With so many people relying on their savings as a source of income, finding the best savings account has never been so important.Ìý

FAQs

What is Annual Percentage Yield?

Annual Percentage Yield (APY) is the effective annual rate of return that takes into account the effect of compounding interest. Unlike the simple interest rate, APY gives a more accurate picture of how much you’ll earn or owe over a year, as it accounts for the frequency with which interest is added to the balance.

What is the role of the Bank of England?

The Bank of England (BoE) is the central bank of the United Kingdom. Its primary roles include setting interest rates to control inflation, issuing currency, overseeing other banks, and working to maintain overall monetary stability within the UK. Through these actions, the BoE plays a crucial role in promoting economic well-being and financial security.

How does compound interest work?

Compound interest is when you earn money not just on the amount you originally put in, but also on the money that you've already earned from that original amount.

What is the consumer price index?

The Consumer Price Index (CPI) is a measure that examines the average price of a basket of consumer goods and services purchased by households. It’s a significant indicator of inflation, as it shows the change in the cost of living over time. When the CPI rises, it indicates a period of inflation, and when it falls, it signifies a period of deflation.

What is an emergency fund?

An Emergency Fund is a savings account that is used to set aside funds to cover unexpected expenses or financial emergencies. This could include house maintenance issues, car repairs, or an unexpected job loss. Having an emergency fund provides financial security and peace of mind as it allows individuals to cover unexpected expenses without having to rely on credit or loans. For more insight into savings accounts, visit our UK savings account statistics page.

Methodology and sources

About Lucinda O'Brien

Lucinda is a senior finance editor at money.co.uk and helps people to make confident financial decisions so they can make the most of their money.