Moving house is expensive - especially if you need to buy a lot of furniture to fill it, you need to equip a kitchen or you have some home improvements to pay for. A 0% purchase card can let you spread the cost of these purchases interest-free.

- >

- Credit Cards>

- Purchases credit cards

Compare our best 0% purchase credit cards

Spread the cost of your spending interest free with a 0% purchase credit card

Make large purchases and save on interest

Find a 0% purchase credit card in minutes

We've partnered with Uswitch to help you find a great deal. Start your eligibility journey now

1

Answer a few basic questions about your circumstances

2

We'll show you the cards youâre likely to get, so you can apply with confidence

3

Your credit score will always be protected

What is a 0% purchase card?

A 0% purchase credit card lets you spread the cost of your spending over several months without paying any interest.

For example, if you use a 0% purchase card with a 20-month interest-free period to buy something for ÂĢ1,500, you could pay it off in equal instalments of ÂĢ75 per month â without any added interest.

Interest-free periods can vary, typically lasting anywhere from three to 21 months. The exact length youâre offered will depend on your credit history and financial situation.

Once the 0% period ends, any remaining balance will start accruing interest at the cardâs standard rate, so itâs best to clear your debt before then to avoid extra costs.

Why get a 0% purchase credit card?

![If you're moving house]()

If you're moving house

Moving house is expensive - especially if you need to buy a lot of furniture to fill it, you need to equip a kitchen or you have some home improvements to pay for. A 0% purchase card can let you spread the cost of these purchases interest-free.

![If you're planning a big holiday]()

If you're planning a big holiday

Getting a 0% purchase card ahead of a big trip abroad can let you pay for flights and accommodation, then pay back the money in instalments over the introductory period. You also get extra refund rights if your holiday is cancelled thanks toĖýSection 75 of the Consumer Credit Act.

![If you're getting married]()

If you're getting married

Weddings are one ofĖýthe most expensive days of your life but are planned months in advance. Interest-free purchase cards come into their own when you know you'll be spending a lot of cash in a short amount of time and want to split that cost over months or even years to come. In many ways, it's a perfect match.

![If you're having a baby]()

If you're having a baby

Equipping a nursery and buying car seats, cots, prams and baby monitors - you can get all of this ahead of time and then pay back the sum in interest-free instalments, keeping costs manageable.

Why get a 0% purchase credit card?

If you're moving house

If you're planning a big holiday

Getting a 0% purchase card ahead of a big trip abroad can let you pay for flights and accommodation, then pay back the money in instalments over the introductory period. You also get extra refund rights if your holiday is cancelled thanks toĖýSection 75 of the Consumer Credit Act.

If you're getting married

Weddings are one ofĖýthe most expensive days of your life but are planned months in advance. Interest-free purchase cards come into their own when you know you'll be spending a lot of cash in a short amount of time and want to split that cost over months or even years to come. In many ways, it's a perfect match.

If you're having a baby

Equipping a nursery and buying car seats, cots, prams and baby monitors - you can get all of this ahead of time and then pay back the sum in interest-free instalments, keeping costs manageable.

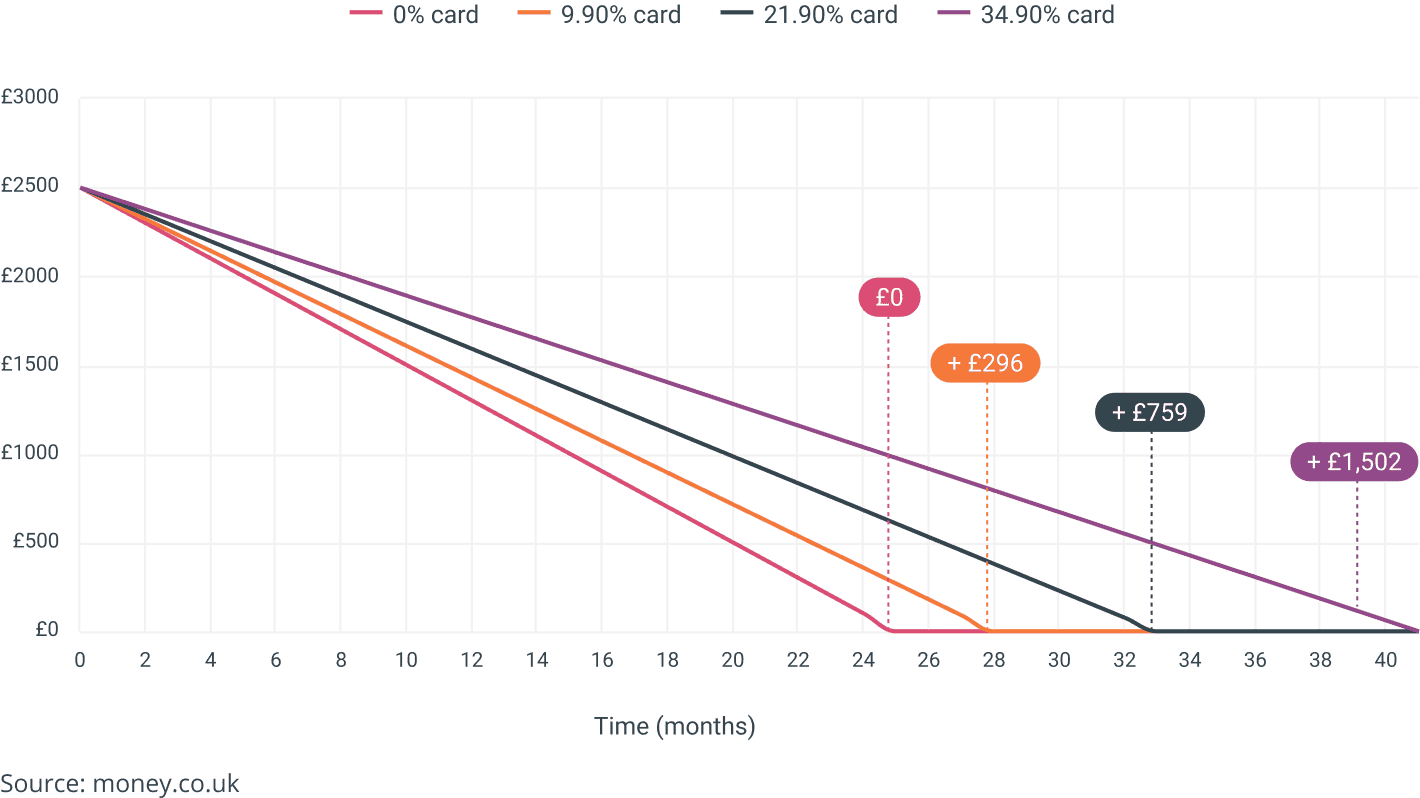

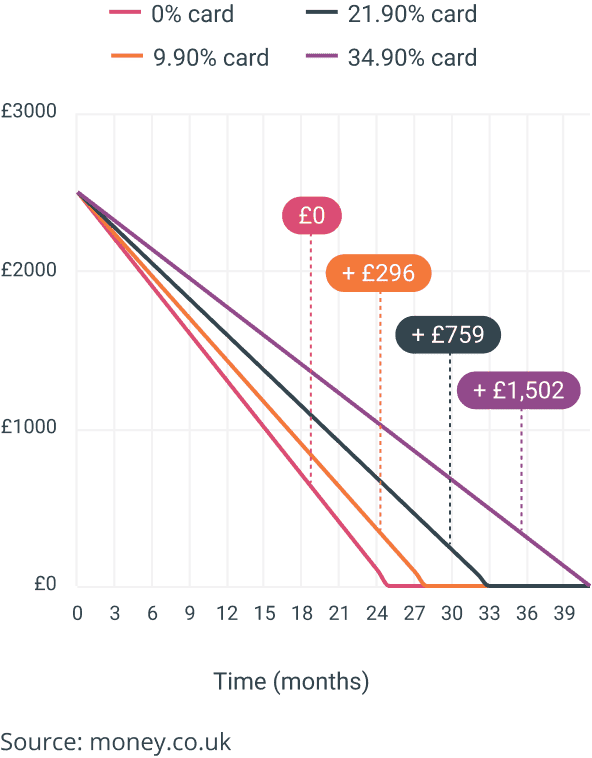

How much interest can you save with a 0% purchase card?

How an interest-free purchase card changes what you pay back and how fast you clear a balance of ÂĢ2,500, assuming a fixed monthly payment of ÂĢ100.

How to choose a 0% purchase credit card

When trying to pick the best 0% purchase card, there are three main features you need to consider.

The interest free period

This is the 0% interest period during which you donât pay any interest on your balance. Ideally, youâll want to choose the longest 0% interest period you can be accepted for. That way, you can pay off your balance over a more extended period and keep your monthly payments as low as possible.

The APR

This is also known as the revert rate, or the interest rate youâll be charged once the 0% interest period ends. If you plan to continue using the card after the 0% deal ends, youâll want the revert rate to be as low as you can get. This is especially true if youâre likely to have a revolving balance on the card i.e. a balance you carry over from one month to the next.

Fees

Some credit cards may charge fees for different kinds of transactions. For example, foreign transaction fees for using the card abroad. Or cash advance fees for using your card to withdraw cash from an ATM. If youâre unlikely to use your card for any of these transactions, these fees shouldnât matter. But if you are, make sure you look for a card with low or zero fees.

What sort of interest free purchase cards are available

![Combination 0% purchase cards]()

Combination 0% purchase cards

Combination 0% purchase cards offer an interest-free period on both purchases and balance transfers. You need to be careful here as the two 0% periods do not always match, and the balance transfer element can come with a transfer fee.

![Rewards 0% purchase cards]()

Rewards 0% purchase cards

Some 0% purchase cards come with rewards for spending on them, meaning you get to spread the cost of your purchases interest-free and get a bonus on top. Rewards for spending can include supermarket points, Avios and even straight-up cash back.

![Bad credit 0% purchase cards]()

Bad credit 0% purchase cards

A few 0% purchase cards are available for people with relatively low credit scores. These typically offer shorter 0% periods - typically between three and six months - and lower credit limits than prime cards. But they can be a valuable option for those without an excellent credit score.

What sort of interest free purchase cards are available

Combination 0% purchase cards

Combination 0% purchase cards offer an interest-free period on both purchases and balance transfers. You need to be careful here as the two 0% periods do not always match, and the balance transfer element can come with a transfer fee.

Rewards 0% purchase cards

Some 0% purchase cards come with rewards for spending on them, meaning you get to spread the cost of your purchases interest-free and get a bonus on top. Rewards for spending can include supermarket points, Avios and even straight-up cash back.

Bad credit 0% purchase cards

A few 0% purchase cards are available for people with relatively low credit scores. These typically offer shorter 0% periods - typically between three and six months - and lower credit limits than prime cards. But they can be a valuable option for those without an excellent credit score.

Our best purchase credit card deals

Our editors have picked out some of our best 0% purchase card deals.

Editorâs pick

Our chosen dual credit card

This credit card is available to new HSBC customers and there are no annual or monthly fees. You also get 0% balance transfers for 17 months, 0% on purchases for 18 months, and a host of exclusive discounts and offers through HSBC Home and Away.â

HSBC Purchase Plus Credit Card

Purchases term

0% for 20 months

Rep APR

24.9% APR

Representative example: The standard interest rate on purchases is 24.9% p.a. (variable), so if you borrow ÂĢ1,200 the Representative APR will be 24.9% (variable).

Show Details

Eligibility

Minimum Age

18 years

Minimum Income

ÂĢ6,800

We are classed as a credit broker for consumer credit, not a lender.

How much can I borrow with a 0% purchase card?

The amount you can borrow depends on yourĖýcredit limit. This is the maximum amount your provider is willing to let you borrow on your credit card, and it will depend on factors such as your credit history, your income and how much debt you already have.

The credit limit of a credit card can range from just a few hundred pounds to tens of thousands of pounds. You can borrow any amount at any time within this limit.

Most credit card providers wonât tell you your credit limit until after youâve applied for your card and theyâve assessed your suitability for the card youâve chosen.

Average credit limit October 2024[1]

ÂĢ5765

How does our eligibility checker work?

Our eligibility checker matches you with the credit cards you're likely to get based on your needs and circumstances. It uses a âsoft searchâ credit check, so your credit score will not be affected.

It's a good idea for most people to use an eligibility checker because it ensures that you only apply for the cards you can get, which means you wonât hurt your credit score through rejected applications

Find a 0% purchase credit card in minutes

We've partnered with Uswitch to help you find a great deal. Start your eligibility journey now

1

Answer a few basic questions about your circumstances

2

We'll show you the cards youâre likely to get, so you can apply with confidence

3

Your credit score will always be protected

What to think about before applying for a 0% purchase card

Will it arrive in time?

If you're trying to snap up a great deal on a new bike, for example, you need to ask yourself if your card will arrive before the offer on the bicycle expires. Most credit cards arrive within 10 working days after your application is accepted, so if thatâs too late, you could end up paying more. 0% purchase cards work best when you know in advance that you'll be spending big and can plan for it.

Make a plan to pay it off

0% purchase cards are not free money. In fact, if you don't clear your balance before the introductory 0% period ends, they can become quite expensive as interest will be charged on your remaining balance. Make sure you know how you'll be paying the card off and how long you have to do it before you start spending.

Find your limits

Once you know your credit limit, make absolutely sure you don't go over it. Missing a payment or breaching your credit limit could mean you fall foul of the card's terms and conditions, and you could lose your 0% period on your entire balance.

What are the alternatives to a 0% purchase card?

Before deciding whether a 0% purchase card is right for you, itâs important to consider the alternatives.

Personal loan

If you need to borrow a fairly large sum of money, say ÂĢ10,000, youâre unlikely to be able to use a credit card as most credit limits wonât stretch far enough. A better alternative could be a personal loan which will let you borrow a lump sum of money (often up to ÂĢ25,000) over a set term of say one to five years.Ėý

Your monthly repayments will be fixed, not flexible as they are with a credit card, but this can make personal loans better for those who need to budget. Youâll also need to pay interest on your repayments, but interest rates can be competitive for sums of between ÂĢ7,500 and ÂĢ15,000.

Overdraft

If you only need to borrow from time to time and your borrowing requirements are fairly small, another option is an overdraft. If you donât already have an overdraft on your current account, applying for one is usually straightforward and your overdraft will often be ready to use instantly. Itâs best to look for an overdraft thatâs interest-free, otherwise rates can be high. If you canât get an interest-free overdraft, aim to pay off your overdraft as soon as possible.

Money transfer credit card

A third option is to use a 0% money transfer credit card. This enables you to move money from your credit card into your bank account. You can then use these funds to pay for a purchase or pay off debt. Interest-free periods can last several months, but youâll usually need to pay a transfer fee of up to 4%. Remember that if you donât pay off your balance in full before the 0% deal ends, interest will kick in.

Watch our video on how 0% purchase credit cards work

Can you get a 0% purchase card with bad credit?

A less-than-perfectĖýcredit ratingĖýdoesn't mean you'll automatically be rejected for cards - but it can limit your choices.

Each provider makes up its own mind about what it considers important when looking at an application. That means even if you've been rejected by one credit card provider, you might not be rejected by another. But a rejection letter or email from one card provider shouldĖýabsolutely notĖýbe seen as a signal to apply to everybody else.

Card lenders share details of who's applying for what with each other â lots of applications in a short space of time can make you look desperate for cash and that will actively hurt your chances of being accepted.

The key is to use anĖýeligibility checkerĖýbefore applying to see what you're more likely to be approved for. People with betterĖýcredit scoresĖýwill generally qualify for more cards, with longer 0% purchase periods.

You will see the number of deals and the length of the interest-free periods go down the worse your credit score gets. But even with aĖýbad credit rating, you might still find someone willing to offer you a deal.

Interest free purchases card jargon buster

APR

APR stands for âAnnual Percentage Rateâ and is the total cost of borrowing over 12 months. For example, if your APR is 20%, you will be charged 20p for every ÂĢ1 borrowed over the course of 12 months. If you pay your balance in full and on time, you will not payĖýinterest.

Annual fee

Some credit cards come with an annual fee, which you pay to use the card. This is separate from interest charges on balances. The fee is charged once a year and typically appears as a one-time fee on your credit card statement.

Cash withdrawal

Withdrawing money from an ATM on a credit card is known as aĖýcash advance,Ėýand it nearly always attracts a cash withdrawal fee, usually of around 3%. In addition, interest is charged on cash withdrawals from the day you take the money out, sacrificing your standard interest-free period.

Several other transactions - including buying stocks and shares, foreign currency and lottery tickets - are frequently treated asĖýâcash-likeâĖýtransactions by card providers and have the same rules and fees applied to them.

Credit limit

Your credit limit is the amount you can borrow on your credit card at any one time. If you exceed this amount, you can be charged a fee - typically ÂĢ12 - and it can leave a mark on your credit report.

You wonât usually find out your credit limit until the end of an application process - although you can ask your provider to increase â or decrease â your credit limit at any time.

Credit limits are set based on your credit history and your earnings.

Once you've reached your credit limit, you need to make a payment to bring down your balance before you can use the card again. Find out more in ourĖýguide to credit limits.

Credit score

Your credit score is calculated based on your credit history. EachĖýcredit reference agencyĖýhas its own method of calculating this.

Your credit score will go up for things like making payments on time and down for things like being late or defaulting on a loan. Typically, the higher your score, the more likely you are to be offered a lower rate of interest or higher credit limit.

There is no absolute pass or fail mark attached to a credit score, with each lender making its own decision on what it considers acceptable.

Direct Debit

A Direct Debit is when you give a company permission to take payments automatically from your bank account. It decides the amount, but you are free to cancel the arrangement. For example, you can set up a Direct Debit to pay off your credit card. This could be for the minimum amount due, a fixed sum, or the entire balance.

Eligibility criteria

Minimum eligibility criteria define the attributes the provider expects customers to have before offering them a product. Theyâre designed to help customers understand if they should proceed with an application.

Meeting the minimum eligibility criteria is not a guarantee of approval. Eligibility criteria include factors such as age, salary and sometimes other details, depending on the product.

Foreign transaction fees

If you buy something abroad or from an overseas website, you are likely to be hit with a foreign transaction fee, which is often around 3% of the total payment.

Some credit cards charge no foreign transaction fees and are designed for use abroad. However, cash withdrawals tend to incur an additional cost, whether at home or abroad. The exchange will be based on Mastercard or Visa currency rates (depending on who issues your credit card).

Interest-free credit

Interest-free credit cards allow you to eitherĖýtransfer a balance, make purchases orĖýtransfer cash to a current accountĖýwithout paying any interest on your balance for a set period. However, you must keep making at least the minimum monthly repayment during this time.

Once the 0% deal is over, you will be charged interest on any remaining debt at your standard APR.ĖýWith balance transfers and money transfers, you will usually have to pay a transfer fee.Ėý

Introductory offer

Credit card introductory offers include bonus reward points, extra cashback, 0% on balance transfers or 0% on purchases.

Introductory offers are used to attract new customers, but once they expire, they revert to the standard offer or rate. When this happens, you should check if youâre still getting the best deal or whether you need to switch to a different credit card.

0% purchase card FAQs

How long will it take to get a card?

It usually takes around 10 days for your card to arrive once you have applied. Here isĖýhow long it can take and how to speed up the process.

Does my credit record matter?

Yes, your credit record matters as itĖýhelps lenders decide whether to accept youĖýas well as what APR and credit limit they will offer you.

How do I repay my credit card?

The best way to repay your credit card is to set up a Direct Debit to pay off the full balance. This means you will never miss a payment or pay interest.ĖýHere are all the ways to repay.

What are minimum payments?

Your provider will setĖýa minimum amount you have to pay back each month. However, itâs best to pay off more than this if you can. If you donât meet the minimum payment, you will be charged a fee of around ÂĢ12, and the missed payment will be noted on your credit record.

Can I do a balance transfer with a 0% purchase card?

No, you can't do a balance transfer unless it is to a combined balance transfer and purchases card. If you do this, you can transfer what you owe on a credit card to a new deal with a better interest rate.

About the author

Didnât find what you were looking for?

Below you can find a list of our most popular credit cards:

Customer Reviews

by 1,066 people

Amazing experience even though itâĶ

Amazing experience even though it wasn't something you would normally deal with, Raaja was super helpful

Natasha Retzmann

Got a great savings account fromâĶ

Got a great savings account from money.co.uk

Raj

Money.co.uk has helped provide the mostâĶ

Money.co.uk has helped provide the most up to date and accurate information Iâve been looking for on mortgages and investing - super helpful

Tom

Weâve been featured in

References

1. UK Credit Card Market Report October 2024