- >

- Savings accounts>

- UK Savings Statistics 2024 - Saving Facts and Stats Report

UK savings statistics 2024

This page includes UK savings statistics for 2024. It looks at different ways people can save money, how much UK adults have on average in savings and the best apps for saving money.

UK savings statistics for 2024 from the Bank of England (BoE) indicate that people deposited ÂĢ8.3 billion into fixed-rate bonds and ISA accounts in August 2023, this was down from ÂĢ10.3 billion in July of the same year.

Savings are a crucial part of money management. Whether itâs putting money aside for a particular purchase in mind, or building up a rainy day pot for something unexpected, comparing savings accounts will ensure you select the one that is right for you.

Our research has gathered the most recent UK savings statistics, encompassing topics such as how much UK households have deposited as savings. The data collected helps reveal what proportion of a personâs income should be saved, along with the reasons why people put money away.

Quick overview of UK savings statistics 2024

The mean average amount of money held in a UK savings account is ÂĢ17,365. ĖýĖýĖýĖýĖý

Up to a third (34%) of adults had either no savings (or less than ÂĢ1,000) in a savings account.ĖýĖýĖýĖýĖý

Around six in 10 (61%) UK adults save money either every or most months.ĖýĖýĖýĖýĖý

Almost two-thirds (65%) of people believe they wouldnât be able to last three months without borrowing money.

Savings accounts are the most popular savings method among UK adults, with over half (57%) using these to save money.Ėý

Men have more savings on average than women across every age group. ĖýĖý

UK savings market statisticsĖýĖýĖýĖýĖýĖý

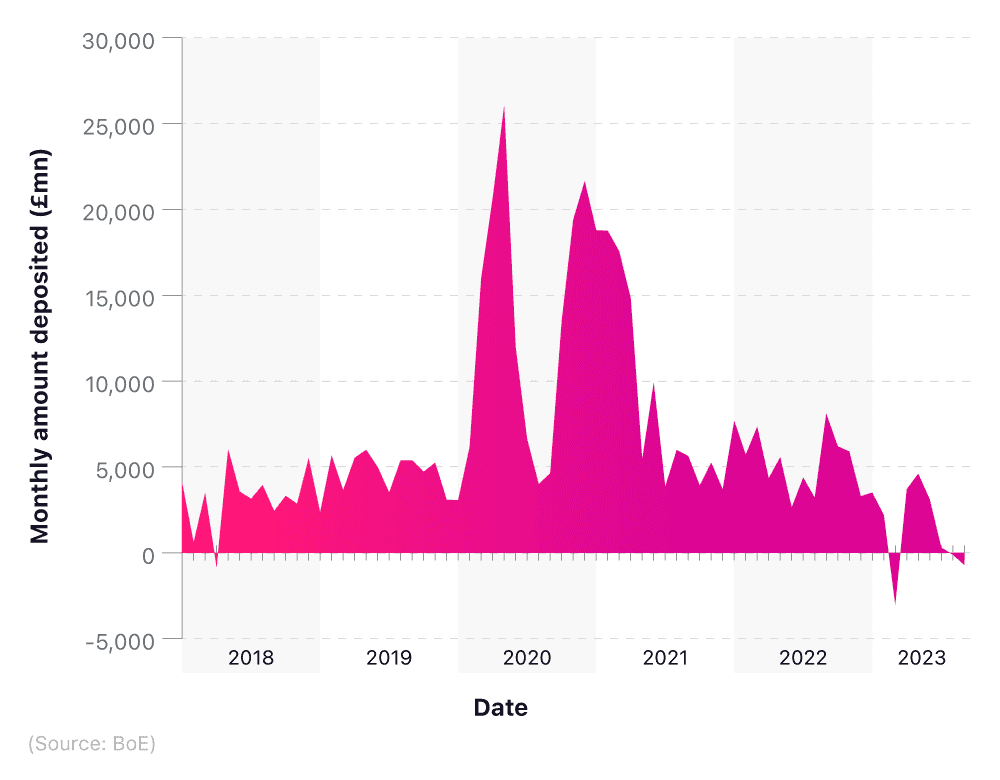

UK savings statistics for 2024 show that UK households deposited a net amount of ÂĢ0.3 billion with banks, building societies and into NS&I accounts in July 2023. The following month, in August 2023, sums deposited were equal to the sums withdrawn, essentially meaning that net deposits were measured at zero. This represents a significant downturn in saving compared to the previous year with the corresponding inflow of deposits for September and October 2022 standing at ÂĢ8.1 billion and ÂĢ6.2 billion, respectively.Ėý

A breakdown of monthly deposits in savings accounts over time

The interest rate on new fixed-rate bonds and ISA accounts for households with banks and building societies increased from 4.94% in July to 5.12%. In the same vein, the rate on existing accounts climbed by 0.24%, from 2.94% in July to 3.18% in August. Additionally, the rate for easy access savings accounts went up from 1.66% in July to 1.83% in August.

During August 2023, net deposits from UK households into National Savings and Investment (NS&I) accounts came to ÂĢ0.3 billion, compared with ÂĢ7.7 billion a month later in September â the highest level since August 2020, when the figure reached ÂĢ9.8 billion. The corresponding figures for September and October 2022 were ÂĢ0.8 billion and ÂĢ0.2 billion respectively.Ėý

The combined seasonally adjusted net flow for both bank and building society deposits and NS&I accounts in August 2023 stood at zero (a decrease of ÂĢ0.3 billion from July), well below the ÂĢ1.5 billion average during the previous six months. For September 2022, the figure was ÂĢ8.9 billion dipping to ÂĢ6.4 billion in October.

For a deeper dive into the condition of the UK savings market, visit our UK savings market trends page for more statistics on average savings and wealth.

How much does an average person have in savings?Ėý

UK savings account statistics revealed that the mean average amount of savings in a UK savings account is ÂĢ17,365. However, as always, average figures hide the gap between the âhavesâ and the âhave-notsâ.Ėý

One in seven (13%) people in the UK revealed they have nothing in their savings, whereas a third (33%) of UK savers said they would struggle to cover a monthâs worth of living expenses if they lost their primary source of income.Ėý

As of Q3 2021, UK households saved an average of 8.3% of their post-tax income (including benefits), which was down from 12.4% in Q2 2021 and 22.8% in Q2 2020.Ėý

Between 2000 and 2015, the UK rate of savings fluctuated between 7-10%, with a recent, pre-Covid peak of 12% in Q1 2010.Ėý

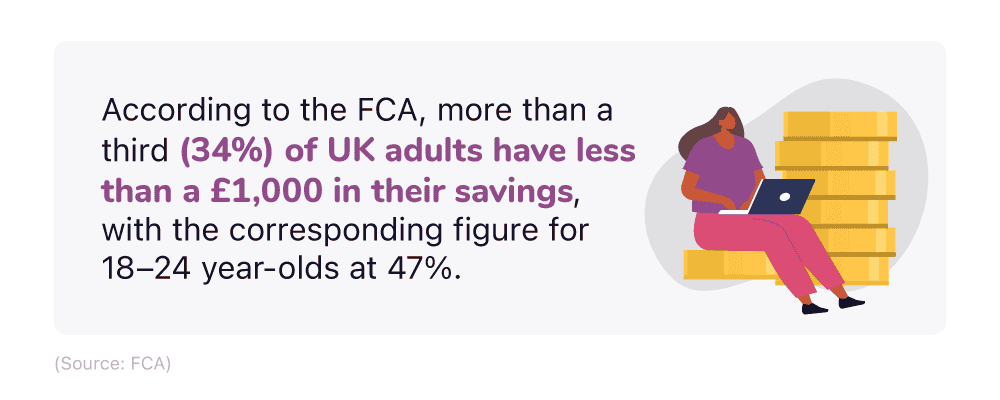

According to savings stats from the FCA, up to a third (34%) of UK adults had either no savings, or less than ÂĢ1,000 in a savings account. This equates to around 22.8 million people with very little or no money to fall back on. This figure was skewed towards the younger population, with under half (47%) of 18-24 year-olds having less than ÂĢ1,000 in their savings account.

According to a survey by the Money and Pensions Service (MaPs), around a quarter of UK adults (11.5 million people) have less than ÂĢ100 in their savings account, with one in six people having no savings at all.Ėý

According to recent credit card statistics, two in five people who use credit are anxious about how much they owe, with over a third worried about the number of different products they already have.

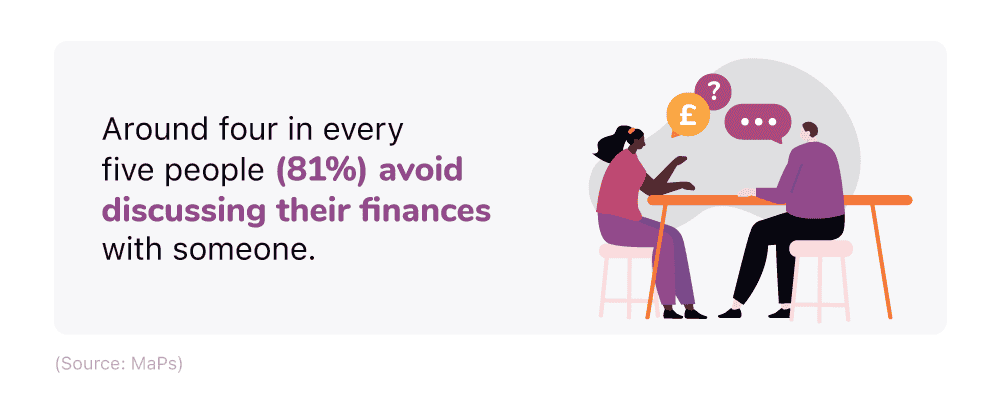

MaPs also found that four in every five people (81%) avoid discussing their finances with someone, with just over a fifth (21%) saying they are fearful of being judged by others. Conversely, just under a fifth (19%) were worried about being a burden to others, with 17% citing shame/embarrassment.Ėý

To align with the MaPs âNation of Saversâ national goal, adults of working age (18-66) are categorised into different groups based on their financial security status, two of which are âThe Strugglingâ and âThe Squeezedâ.

The âstrugglingâ vs. the âsqueezedâ

| âThe Strugglingâ | âThe Squeezedâ |

|---|---|

| Least financially resilient | High-risk category |

| Low income | High rates of dependency on credit |

| High rate of benefit dependency | Lack of savings buffer |

| Poor provision for later life | Not prepared for later life |

| Little or no savings buffer | |

| High levels of debt/over-indebtedness |

(Source: MaPs)

According to the UK Strategy for Financial Wellbeing, there are 11.1 million adults across the country who fall into one of these two categories. This equates to over half (56%) of all working-age adults in the UK, and 61% of the total adult population, who are classed as inadequate savers.Ėý

The national target is to encourage two million more people to save regularly by 2030.

Other aims of the UK strategy for financial wellbeing include:

Reducing the number of people often using credit to buy food and pay bills by two million

Ensuring that five million more people understand enough to plan for and cope in later life.

If youâre looking to save more money, but not sure how, our guide to financial advisor help could help point you in the right direction and help in setting your savings goals.Ėý

How much should people save?

Managing your savings is a highly personalised process. How much you save will depend on the specific reason for saving and the associated time frame.Ėý

Less than a year - can be used to target a holiday, buy a specific gift, or pay one-off, larger bills (e.g. car insurance).Ėý

Less than a decade - might be to cover the cost of large expenditures, such as making a downpayment on a house or replacing something significant that breaks (e.g. a boiler).Ėý

Lifetime - putting money away for retirement through a lifetime ISA account, for example.Ėý

Generally speaking, between 10-15% of your income should go towards a comfortable retirement fund. If you have employer contributions, then this can help reduce the burden (i.e. they contribute 5% and you contribute 5%).Ėý

As a rule of thumb, you should establish an emergency fund that can cover up to nine months of your living expenses. This is to account for loss of income should you lose your job, yet still allows you to cover your basic survival costs (i.e. accommodation, bills, food etc.).Ėý

Another theory is to follow the 50/30/20 rule, where:

50% of your income should go towards necessities (i.e. needs).Ėý

30% goes towards desirable purchases (i.e. wants).Ėý

20% goes into a savings account (either retirement, emergencies, or a particular financial goal).Ėý

Using this method, up to half of your money is fixed on the non-negotiable aspects of living that you cannot avoid paying out for, such as mortgage/rent, household bills, and groceries.Ėý

You may opt for more than 20% towards savings, which is fine and could benefit you in the long run. But any less, and this may mean a longer saving period towards your ultimate saving goals.Ėý

The other way to view this is to consider your age bracket. Here is a rough estimate of how much you should be putting into retirement savings by decade, based on the average annual UK wage of ÂĢ32,292, as of November 2022.Ėý

How much of your salary should you save? (Exclusive data)

| How much of your salary you should save (by decade) | Amount of savings |

|---|---|

| 1 x your salary by the age of 30 | ÂĢ32,292 |

| 3 x your salary by the age of 40 | ÂĢ96,876 |

| 6 x your salary by the age of 50 | ÂĢ193,752 |

| 8 x your salary by the age of 60 | ÂĢ258,336 |

The bottom line is, there is no hard-and-fast rule with regards to how much people should save. Whether itâs 5%, 20%, or more, putting money away today will help prepare you for a more financially secure future.Ėý

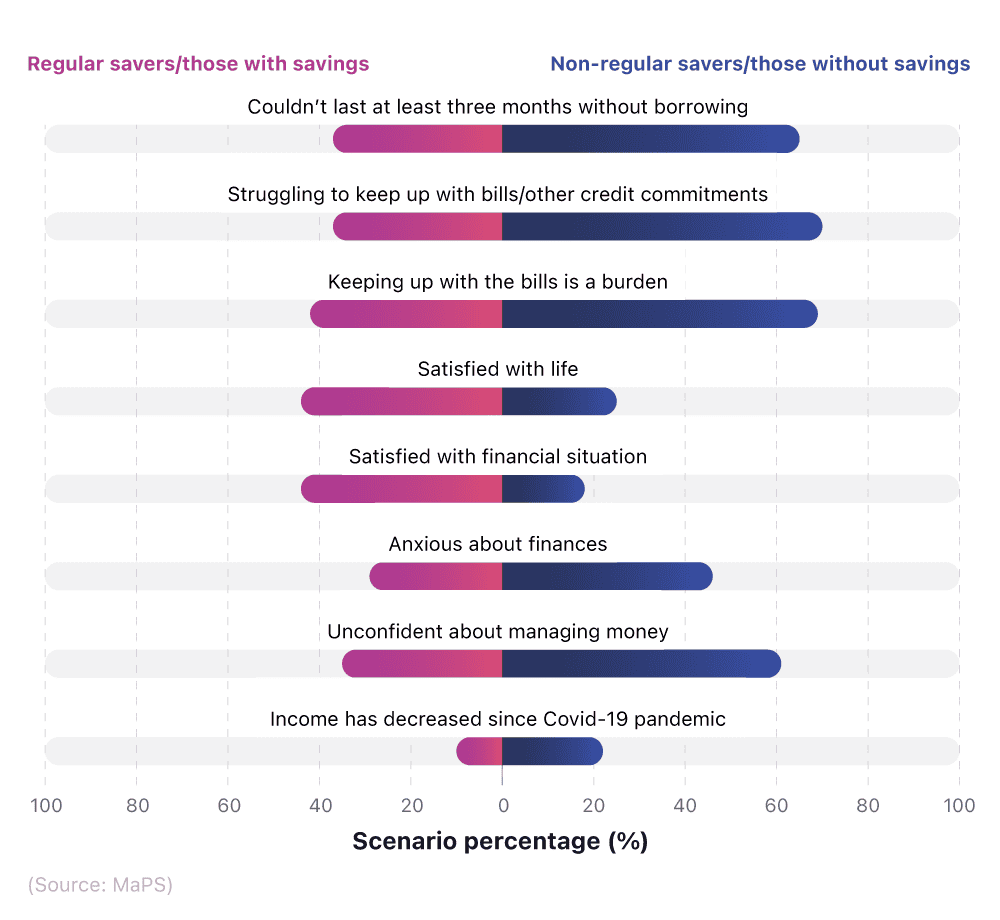

A breakdown of attitudes and feelings between regular and non-regular savers

The Financial Wellbeing Survey 2021 found that 61% of UK adults save money either every, or most, months. These people are defined as âregular saversâ.Ėý

Those in the habit of not saving regularly are much more likely to experience financial issues in other areas of their lives, including:

Susceptibility to a dramatic reduction in income, with almost two-thirds (65%) claiming they wouldnât be able to last three months without borrowing money.Ėý

Keeping up with billsâ70% would struggle with this, while over two-thirds (69%) would find it a burden.Ėý

Reduced happinessâa quarter (25%) of non-savers feel less satisfied with life, and less than a fifth (18%) arenât happy with their financial situation.Ėý

Increased anxietyâjust under a third (29%) of those who arenât saving regularly claim they feel more anxious with regards to money.Ėý

Reduced confidence in managing their money, with more than one in six (61%) admitting they no longer feel confident doing so.ĖýĖý

Regular saving provides good financial resilience for your future. Those who do save regularly are:Ėý

Almost twice as likely to be able to cope with a significant loss of income and keep up with paying bills, as well as less likely to find this a burden (42%).

More satisfied with their life as a whole (44%).

Less anxious about finances (29%).

Almost twice as confident in managing their money compared to non-savers.Ėý

Why do people save money?Ėý

The majority of UK adults (57%) have savings in place for no particular purpose, and are just accumulating money to use sometime in the future (i.e. a rainy day).Ėý

Reasons why people save moneyĖý

| Reason why people save | Percentage of people who save for this reason (%) |

|---|---|

| For a rainy day | 57% |

| Unexpected expense or events | 44% |

| Planned expense or events | 35% |

| Retirement (excluding pension) | 26% |

| In case household income changes | 21% |

(Source: MaPs)

Just under half (44%) are saving for unexpected expenses or consequences should it happen, compared to just over a third (35%) who are saving with a specific event/expense in mind.Ėý

Slightly more than a quarter (26%) are using their savings to supplement their retirement, with just over a fifth (21%) safeguarding for the future should their income change.Ėý

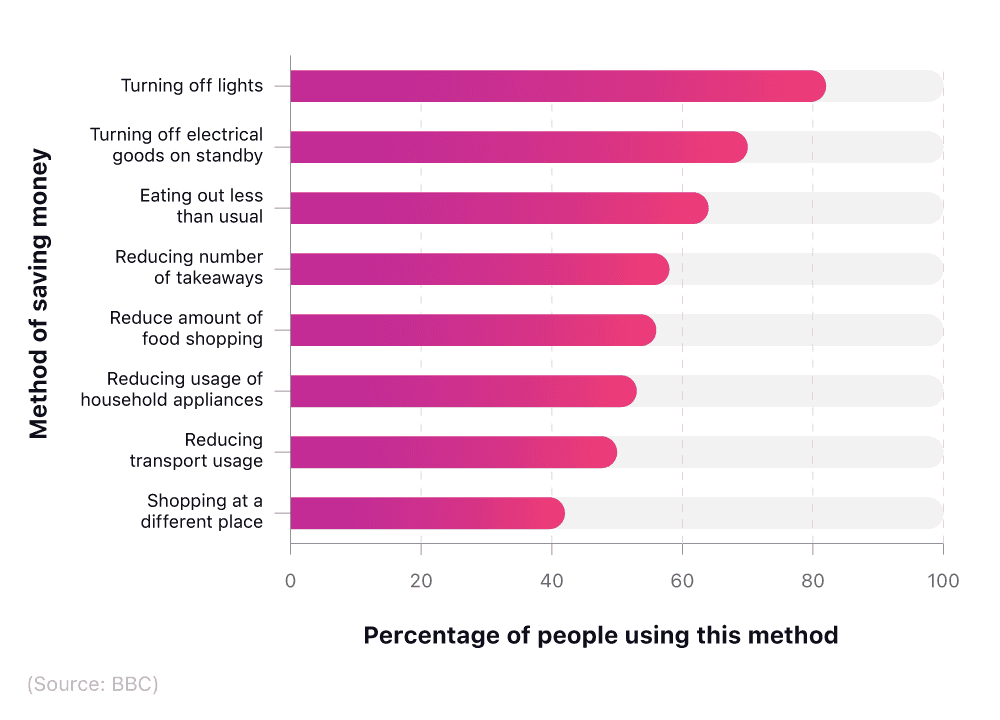

Other ways to save moneyĖý

As of June 2022, 82% of people surveyed across the UK were turning off lights in a bid to save money during the cost of living crisis. This was the most popular method for saving money, followed by turning off electrical goods on standby (70%) and eating out less than usual (64%).Ėý

A breakdown of different ways of saving money and the percentage of UK people who use that method

More than half of people stated they were looking to reduce their consumption habits, such as takeaways (58%), food shopping (56%), and household appliance usage (53%).Ėý

A breakdown of the best apps for saving money (exclusive data)

| App | Monthly global downloads (Android) | Monthly global downloads (iOS) | Total global downloads |

|---|---|---|---|

| Revolut | 700,000 | 600,000 | 1,300,000 |

| Idealo | 400,000 | 300,000 | 700,000 |

| Monzo | 100,000 | 100,000 | 200,000 |

| Starling Bank | 30,000 | 70,000 | 100,000 |

| Plum | 40,000 | 40,000 | 80,000 |

| Monese | 50,000 | 30,000 | 80,000 |

| Topcashback | 30,000 | 50,000 | 70,000 |

| Moneybox | 10,000 | 40,000 | 50,000 |

| Quidco | 20,000 | 20,000 | 40,000 |

| Emma | 10,000 | 20,000 | 30,000 |

| Snoop | 10,000 | 10,000 | 20,000 |

| Raisin | 9,000 | 9,000 | 18,000 |

| HyperJar | 7,000 | 9,000 | 16,000 |

| Beanstalk | <5,000 | <5,000 | <10,000 |

| Chip | <5,000 | <5,000 | <10,000 |

| Sprive | <5,000 | <5,000 | <10,000 |

| CheckoutSmart | <5,000 | <5,000 | <10,000 |

| Vouchercloud | <5,000 | <5,000 | <10,000 |

| Youtility | <5,000 | <5,000 | <10,000 |

(Source: money.co.uk via Sensortower via 42matters.com)

Of all the available apps for saving money, Revolut sits at the top in terms of global downloads (1.3 million). This is almost twice as many as second-placed Idealo, with 700,000.Ėý

As of December 2022, Monzo is the third most popular downloaded app for saving money, with 200,000 downloads. This is twice as many as fourth-placed Starling Bank, with 100,000. Money management app Plum is in fifth, with 80,000 downloads across Android and iOS devices in 2022.Ėý

Android was slightly more popular than iOS as the source of apps for saving money (1.4 million vs 1.3 million), with around 50% of Android and iOS downloads attributed to Revolut alone.Ėý

Our guide to stocks and shares apps available on the market can help with learning how to choose shares and trade, and run a portfolio from the comfort of your screen.

Glossary

Bank of England (BoE)

The Central Bank of the United Kingdom. It is responsible for setting interest rates and promoting monetary stability.

Consumer Price Index (CPI)

An index measuring the average price of consumer goods and services purchased by households. It is often used to assess inflation.

Interest rate

The amount charged, expressed as a percentage, by a lender to a borrower for the use of money. Interest rates are sometimes considered the reward for saving and the cost of borrowing.Ėý

Fixed-rate savings account

A savings account where the interest rate remains the same for a set period, regardless of market conditions.

Individual Savings Account (ISA)

A class of retail investment arrangements available to residents of the UK, providing a favourable tax status.

Real interest rate

The interest rate once adjusted for inflation, representing the real cost of borrowing or real yield on an investment.

Defined benefit plan

A type of pension plan where an employer promises a specified monthly benefit on retirement. The amount is determined by a formula based on the employee's earnings history, tenure and age.

Government bonus

A monetary incentive provided by the government to encourage saving that is paid on top of the money saved in a Help to Save account.

Payment frequency

The regularity with which savings are deposited into an account â for example, weekly, bi-weekly, or monthly.

FAQs

How much does the average person save per month in the UK?

The average monthly savings deposit for UK households is approximately ÂĢ450. This figure represents the mean savings rate, which is elevated due to a small proportion of households with significantly higher savings rates.

How much does the average person have in their savings account?

The amount of money a person has in their savings account varies and is based on various factors, including age, gender, occupation and spending habits.Ėý According to the Building Societies Association, the mean average savings for someone in the UK is ÂĢ17,365.

How much should you have saved by the age of 30?

The amount someone should have saved by the age of 30 depends on your circumstances and expectations. Some financial advisors suggest that everyone should have an emergency fund that can cover three to six months of living to be financially secure.

Another common guideline is to have the equivalent of your annual salary saved for retirement by the age of 30. For example, if you earn ÂĢ25,000 a year, you should aim to have ÂĢ25,000 worth of savings in your account by your 30th birthday.

How much of your income should you invest?

Itâs advisable to focus on cutting down any debt (if you have any) and building up your savings before investing. Ultimately how much of your income you're willing to invest depends on how comfortable you are with risk.Ėý

If you do decide to invest, you may wish to consider diversifying your investments to reduce risk.

Will UK savings interest rates rise?

In a bid to tackle rising inflation, The Bank of England (BoE) has recently increased its base interest rate to 5.25%, the highest it has been in 15 years. However, with the rate of inflation now beginning to slow, this suggests that a slight reduction in interest rates may come before the end of the year.

Methodology and sources

Ėý

Ėý

Ėý

Ėý

Ėý

Ėý

Apps for saving money

Ėý

Ėý

Read more like UK savings statistics 2022 :

How does the State Pension work?

Not everyone gets a state pension in the UK, and payouts vary heavily from person to person, even for those who qualify. Here is how the state pension works, what it could pay you and when you can claim it.

Read more about how the State Pension works

About Lucinda O'Brien

Lucinda is senior finance editor at money.co.uk and helps people to make confident financial decisions so they can make the most of their money.