- >

- Business Insurance>

- 50+ UK Business Insurance Statistics 2024

50+ UK Business Insurance Statistics 2024

This page includes relevant 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics for 2024, such as claims data and average costs for factors like region, sector, and insurance type.

There are few things more vital to safeguarding a company than business insurance. For generations, business insurance has been the fundamental factor protecting companies from common risks like legal liability, property damage, and financial loss.Â

As the digital world accelerates, many companies now require insurance that protects against modern-day threats, like cyber fraud, as well as traditional, onsite factors such as buildings and contents.Â

Our research has gathered more than 50 of the most prominent 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics for 2024, including information on average costs, the size of the business insurance industry, as well as specific insurance types, like cyber insurance and professional indemnity cover.

Overview: 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics

On average, 91Ïã―ķŧÆÉŦĘÓÆĩinsurers pay out around ÂĢ22 million per day.

Typically, around ÂĢ7.6 million per day is paid out in business liability claims.

The UK commercial insurance market was worth over ÂĢ15.5 billion in 2023 â a 71.8% rise from 2021.

More than half (51%) of small-to-medium enterprises (SMEs) have stopped buying one or more types of business insurance.

The average cost of employers' liability for a single office worker is ÂĢ61 per year â this rises to ÂĢ213 for a manual worker.Â

The average annual cost of public liability insurance in the UK is ÂĢ120.

Over a quarter (26%) of insurance claims made in the UK are related to professional indemnity.Â

Types of business insurance

There are numerous types of business insurance on the UK market covering businesses for various events and circumstances.Â

Many companies will have either a combination of different insurance policies or take out a sole policy combining a range of different business insurance types. The types of business insurance each company requires can depend both on the size of the business and the nature of the work being done.

Some of the most prominent types of business insurance are:

Employersâ liability insurance protects you if one of your employees becomes ill or injured as a result of working for your company. This type of insurance covers both full- and part-time employees, as well as volunteers and freelance or casual workers.

Note: Employersâ liability insurance is a legal requirement in the UK.

Public liability insurance covers your business against any claims from a client or member of the public who has been injured or had property damaged as a result of work carried out by your company.

Professional indemnity insurance covers your business against the cost of compensating clients for loss or damage resulting from negligent services or advice provided by your company.

Commercial buildings insurance covers the costs of repairing and rebuilding of your business premises in the event of adverse events like fires, floods, or storms.

Business contents insurance protects you against losses if assets at your premises are damaged or stolen (e.g. computers or workplace equipment).

Business interruption insurance offers protection against loss of income during periods when you cannot work as normal due to unforeseen circumstances.

Cyber insurance protects businesses against losses incurred from online threats (like cyber fraud and data breaches).

91Ïã―ķŧÆÉŦĘÓÆĩinsurance market statistics

Based on total premiums written, the latest business insurance statistics found that the UK insurance industry is the largest in Europe, and the fourth largest in the world.Â

A report from the Association of British Insurers (ABI) found that UK insurers pay out approximately ÂĢ22 million per day on average for business insurance claims.Â

Of this:

ÂĢ7.6 million per day comes from all liability claims

ÂĢ1.8 million is attributed to employers' liability.Â

Want advice on how to make a claim on your business insurance? Visit our comprehensive business guides for expert tips on this and more.

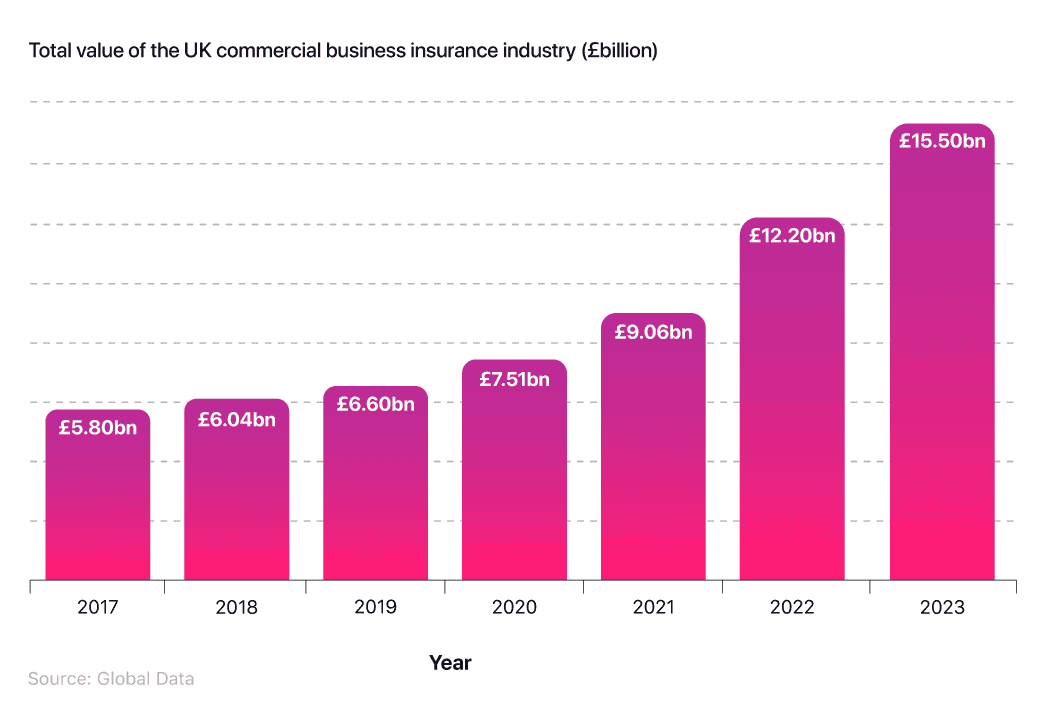

What is the value of the UK commercial insurance market?

The latest 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics found that the UK commercial insurance market was worth over ÂĢ15.5 billion in 2023. This represents an increase of 71.8%, from 2021 when the industry was valued at ÂĢ9.1 billion. Since 2020, the market has grown by 106% from ÂĢ7.51 billion to ÂĢ15.5 billion.

A breakdown of the overall value of the UK commercial buildings insurance industry by year

The industryâs growth accelerated rapidly from 2017, when it was worth less than ÂĢ6 billion. From here, consecutive annual rises of between 3% and 4% occurred before increasing by 9.4% between 2019 and 2020. The latest findings mean that the business insurance industry increased in value by around 167% between 2017 and 2023, enjoying an average annual growth of around 27.8% over this period.

What percentage of UK businesses have business insurance?Â

Recent 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics found that 51% of businesses stopped buying at least one form of insurance cover during 2023. By comparison, in 2022, just over four in 10 (44%) of small-to-medium enterprises (SMEs) didnât have any form of insurance.

Research by the British Insurance Brokers Association also found that, as of 2023, 26% of SMEs stopped buying compulsory employersâ liability insurance, while 22% stopped buying professional indemnity insurance.

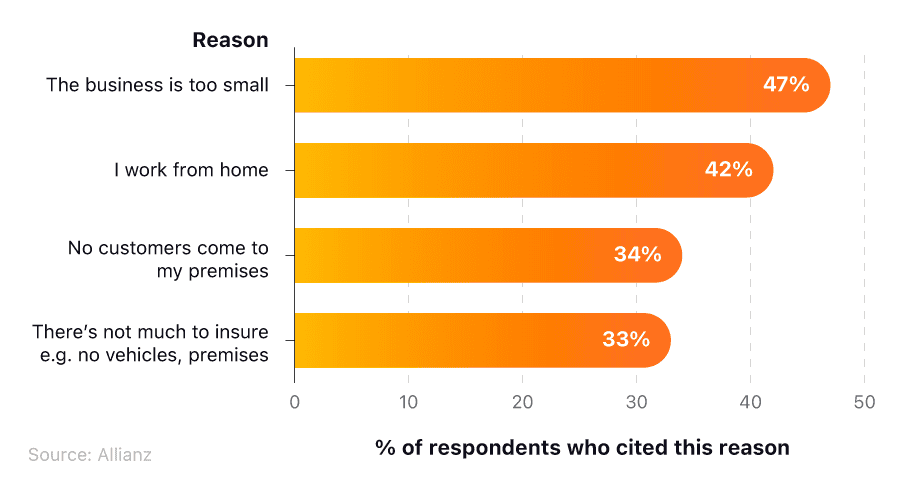

Over 99% of private UK businesses fall into the SME category, which means more than five in 10 have stopped buying one type of insurance. A survey from Allianz found nearly half (47%) of uninsured businesses consider their company too small to warrant an insurance policy.

Breakdown of the most common reasons uninsured businesses give for not having business insurance

A further 42% of respondents cited working from home as the main reason theyâre uninsured, while around a third of people (34%) believed they didn't need insurance because no customers came to their premises.

Elsewhere, a report by Aviva found that around 17% of SMEs may not have employersâ liability (EL) insurance, which is a legal requirement for any business with employees that arenât part of their own family.

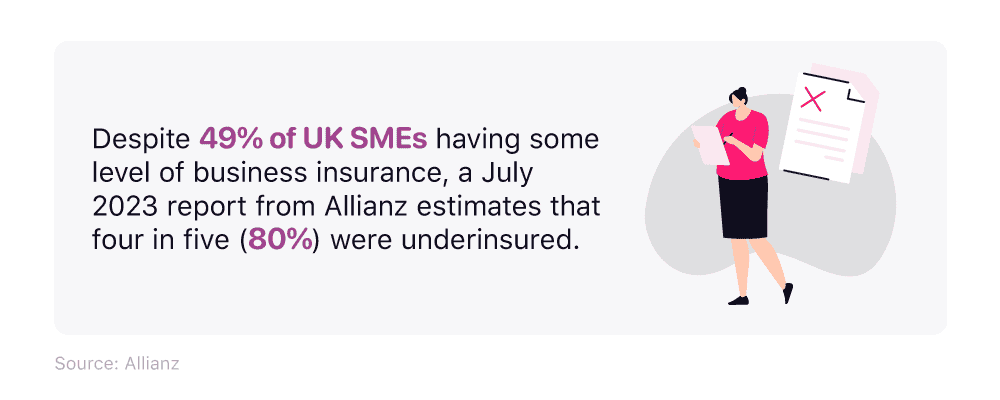

How many businesses are underinsured?

Despite 49% of UK SMEs having some level of business insurance, a July 2023 report from Allianz estimates that four in five (80%) were underinsured. Â

Elsewhere, a report from Aviva also found that around 45% of businesses with building insurance policies have at least one premise likely to be underinsured by 20%.

Various economic factors, such as inflation and supply chain issues, affect the costs required to fully insure your business. Despite this, just under a third (32%) of business owners in Avivaâs survey said they had not considered inflation or supply chain issues when taking out insurance, while a further 28% claimed they had not reviewed their sums insured over the last year.

Additionally, despite almost a fifth (21%) of businesses claiming theyâd experienced business disruption of some kind, 62% said they either donât have business interruption insurance or are unsure whether itâs already included in their policy.

What is the average cost of business insurance in the UK?

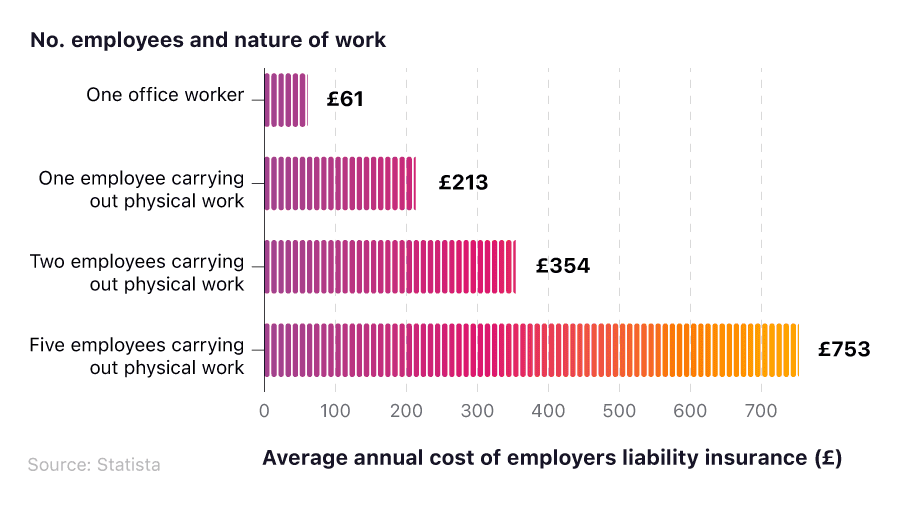

The latest 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics found that the average cost of employersâ liability insurance for a single office worker was ÂĢ61 per year in February 2022. This figure rises by 249% (to ÂĢ213 per year) for any employee carrying out physical work, such as construction.

Breakdown of the average annual cost of UK employersâ liability insurance by number of employees and nature of work

The cost of employersâ liability insurance increases substantially with the number of employees. The average annual price for two employees carrying out physical work is ÂĢ213 â 66% more than the cost for one employee.

Similarly, insuring five physically active workers increases the annual costs to ÂĢ753. This represents a 112% increase compared to insuring two such workers and 254% compared to insuring one.

What is the average cost of public liability insurance in the UK?

According to research from AXA, the average cost of public liability insurance is ÂĢ120 each year. However, this figure can be substantially lower for smaller businesses, with some paying as little as ÂĢ40 for the year.

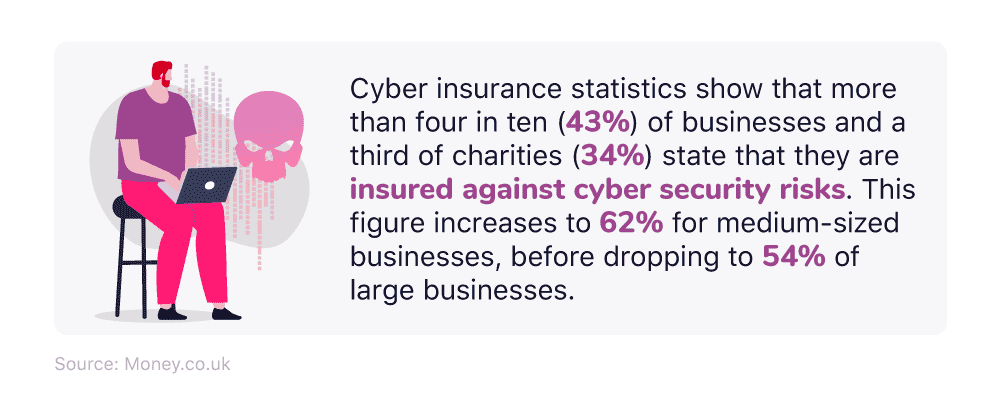

UK cyber insurance statistics

The latest cyber insurance statistics show that fewer than four in 10 (37%) businesses and only a third of charities (33%) state that they are insured against cyber security risks. This figure increases to 63% for medium-sized businesses, before dropping to 55% for large businesses.Â

This is a decrease of 6 percentage points from 2022, when 43% of businesses were protected from cybercrime.Â

In addition, 29% of businesses have undergone cyber-security risk assessments within the last year. For medium-sized businesses, this figure is even higher, increasing to 51%, whilst for large businesses it is 63%.

Despite the high volumes of SMEs not taking out cyber insurance, a British Insurance Brokers Association (BIBA) report found that 96% of cyberattacks are directed at small-to-medium enterprises.

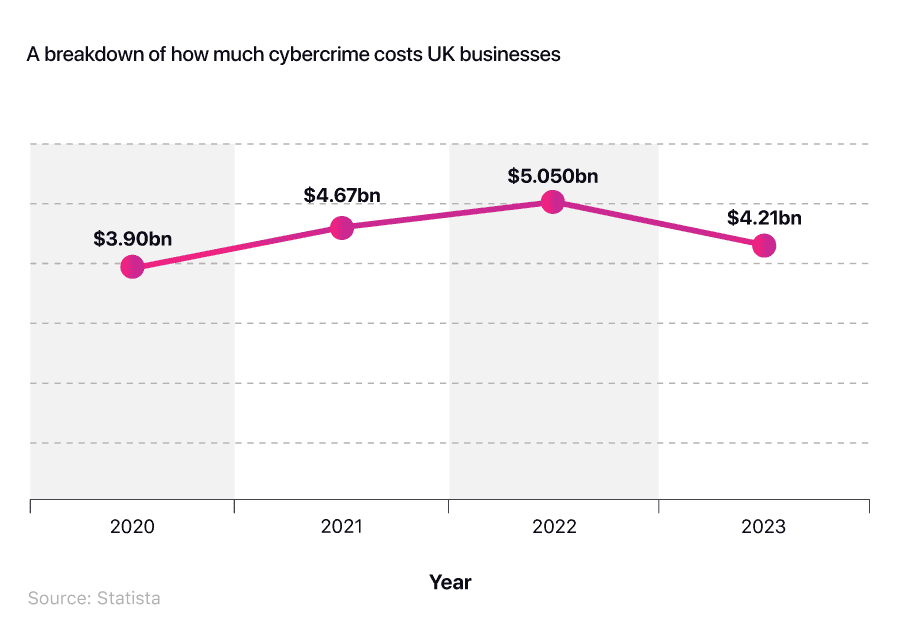

How much does cybercrime cost UK businesses?

The cost of cybercrime increased by close to three-tenths (29.5%) between 2020 and 2022, rising from $3.9 billion to $5.05 billion.

A breakdown of how much cybercrime costs UK businesses

For the first time since 2020, the cost of cybercrime decreased in 2023, reducing by 17% to $4.21 billion. Despite this drop, the overall cost of cybercrime to UK businesses rose by 8% between 2020 and 2023.

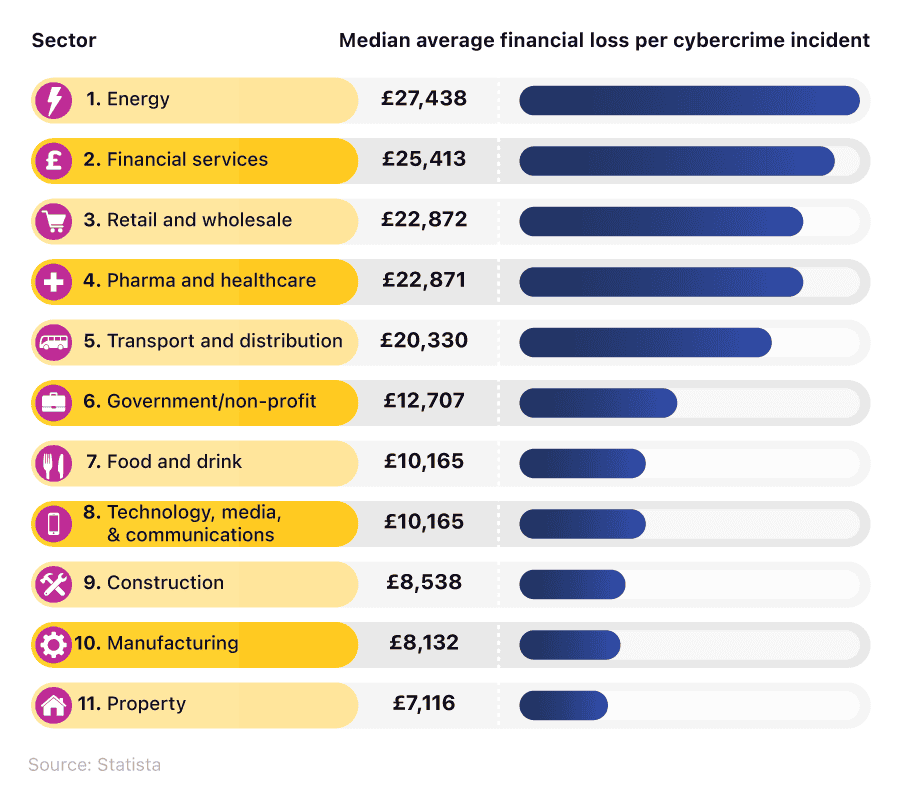

Which UK industries have suffered the most from cybercrime?

The UK energy sector suffers the most cybercrime losses on average. Recent 91Ïã―ķŧÆÉŦĘÓÆĩinsurance stats found that the median average cost of cyber incidents for energy companies was over ÂĢ27,000 in 2021 â 8% more than any other industry.

The financial services industry was the only other sector with an average cybercrime incident cost of more than ÂĢ25,000. The exact figure of ÂĢ25,413 is around 11% more than the retail and wholesale industry (the third most affected sector in the UK).Â

Breakdown of the 10 UK industries that incurred the highest average financial loss per cybercrime incident

Five UK industries incur average cybercrime costs over ÂĢ20,000. These are:

Energy

Financial services

Retail and wholesale

Pharma and healthcare

Transport and distributionÂ

There is a 37% drop in average costs between transport and distribution (ÂĢ20,330) and government/non-profit (ÂĢ12,707), followed by steady decreases in the remaining sectors.Â

Property was the industry with the 10th highest average costs for cybercrime, with its average figure of ÂĢ7,116, around 74% lower than the energy industry, which is in pole position.Â

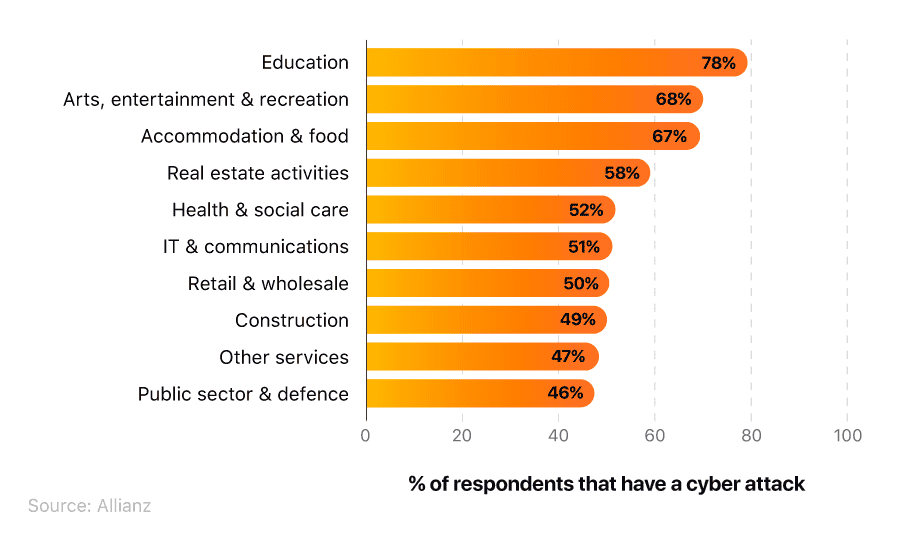

UK sectors that have experienced the most cyber attacks

Education was the industry that experienced the most cyber attacks in the UK, with close to four in five (78%) respondents in this sector stating that theyâd suffered an attack in the last year. This is 10 percentage points more than the next highest, which is arts, entertainment and recreation (68%).

Construction (49%), other services (47%), and public sector and defence (46%) were the most resilient to cyber attacks, with fewer than half the businesses in these sectors suffering attacks in the last year. These were the only sectors where under half of businesses were the victims of cyber attacks.

UK professional indemnity insurance statistics

Recent 91Ïã―ķŧÆÉŦĘÓÆĩstatistics found that professional indemnity-related claims are the most frequent type in the UK. A report from Allianz found that these claims make up more than a quarter (26%) of the annual total.Â

The majority of these are related to issues like:

Loss of money

Professional negligence

Loss of documentation

Breach of copyrightÂ

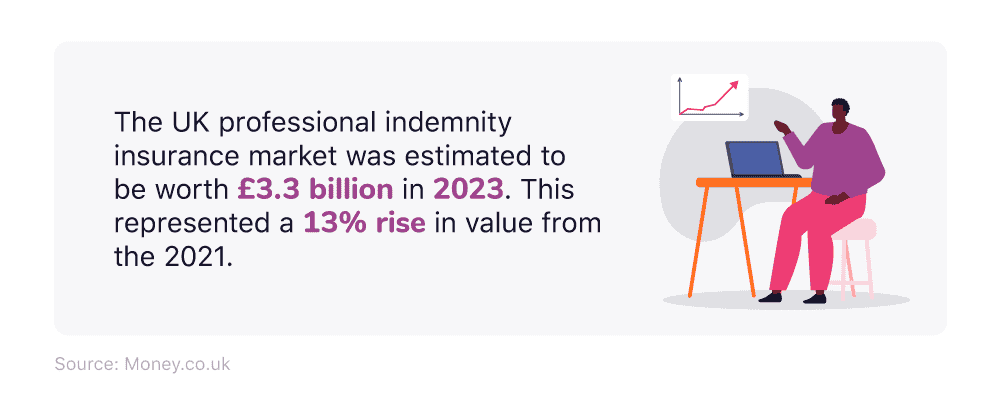

The UK professional indemnity insurance market was estimated to be worth ÂĢ3.3 billion in 2023. This represented a 13.8% rise in value from 2021, when the market was worth ÂĢ2.9 billion. Traditional professions like solicitors, accountants, and financial advisors make up between 75% and 80% of the market, combined.Â

Legal services are among the biggest buyers of professional indemnity policies, with the solicitor market for this type of insurance estimated to be worth around ÂĢ340m. Research shows that law firms typically paid PII premiums between 3% and 9% of their annual turnover in 2023.

91Ïã―ķŧÆÉŦĘÓÆĩclaims statistics

The latest 91Ïã―ķŧÆÉŦĘÓÆĩclaims statistics found that UK insurers paid out ÂĢ179.9 billion in claims in 2020. This accounted for more than a fifth (20.5%) of the entire claims paid throughout Europe that year.

How much do UK insurers pay out for liability insurance claims?

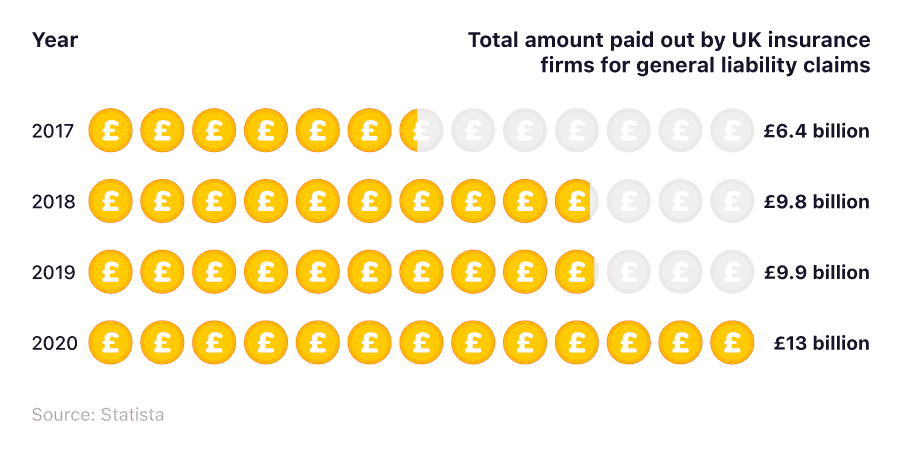

Liability insurance payouts have risen steadily since 2015, with UK insurance firms paying out around ÂĢ13 billion in 2020 alone.

Breakdown of the total cost of general liability claims paid out in the UK by year

Costs accelerated in 2018 when they reached ÂĢ9.8 billion. This represented a 53% rise from the previous year, the highest recorded figure at that time. From here, payouts remained consistent in 2019 before increasing by almost a third (31%) to ÂĢ13 billion in 2020.

This means that the total cost of liability insurance payouts more than doubled (+103%) between 2016 and 2020.

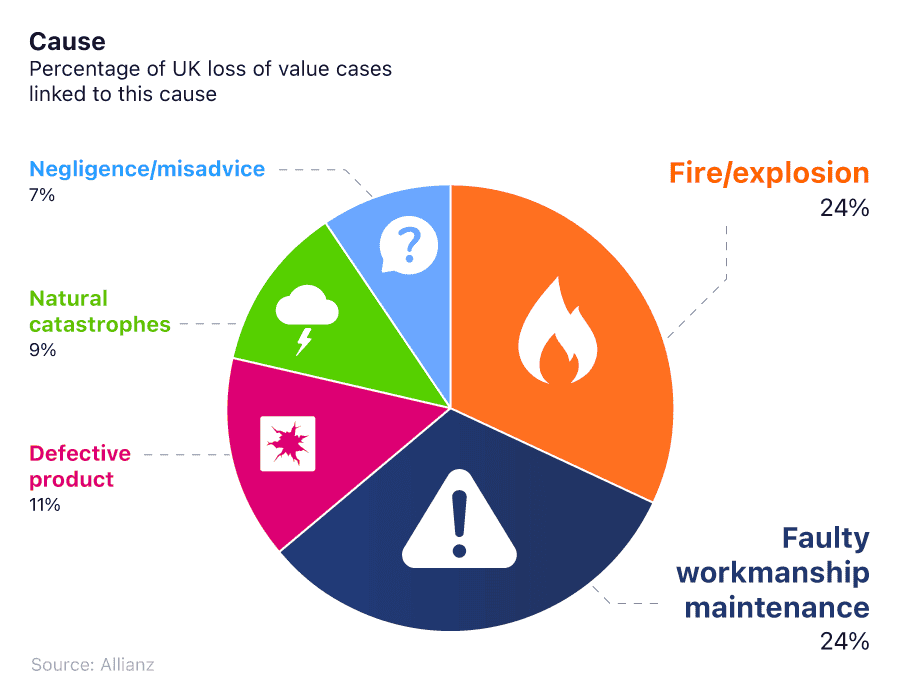

What is the biggest cause of loss of value in the UK?

The latest 91Ïã―ķŧÆÉŦĘÓÆĩinsurance statistics found that fires, explosions and faulty workmanship are the biggest causes of loss of value in UK businesses, which together are responsible for nearly a quarter (24%) of all reported incidents.Â

Breakdown of the most common causes of loss of value to UK businesses

A defective product was the only other reason (11%) cited in more than 10% of claims, with natural catastrophes and negligence/misadvice featuring in 9% and 7% of claims, respectively.Â

Business insurance FAQs

What is business insurance?

Business insurance guards against losses due to events that may happen during the regular course of business. There are many different types of insurance for businesses, including coverage for property damage, legal battles and employee-oriented risks.

What is business interruption insurance?

Business interruption insurance covers against the loss of income during periods when you canât carry out your business work as normal, due to an unforeseen event (e.g. building damage).

Do I need business insurance?

Every small-to-medium enterprise should consider business insurance. Insurance helps protect against potential risks and liabilities, ensures compliance with legal requirements, and safeguards financial stability. Most employers will need to have employersâ liability insurance by law.

Knowing how to claim on your business insurance ahead of time ensures youâre well-equipped to get your business back on track should the worst happen.

How much is business insurance?

The average cost of business insurance varies widely. Policy prices depend on factors such as the type of coverage needed, the size and nature of the business, location, and specific risk factors.

What does business insurance cover?

Business insurance covers potential risks and liabilities such as property damage, legal claims, employee injuries and business interruptions, ensuring financial protection and stability for business.

How much is liability insurance for a small business?

Public liability insurance generally ranges from ÂĢ60 to ÂĢ500 per year, depending on coverage levels, business risk, and the size of the company.

Learn more about public liability for small businesses on our comprehensive guide.

Do e-commerce businesses need insurance?

Yes, e-commerce businesses need insurance to protect against risks such as cyber liability, product liability, general liability and business interruption.

Business insurance glossary

Glossary of terms

Cyber fraud

Cyber fraud is a blanket term that describes crimes committed by hackers and scammers online. These crimes are undertaken to acquire a businessâs sensitive information for monetary gain.

Data breach

A data breach is a security violation in which private information is viewed, stolen, copied or altered by a person without access authorisation.

Loss of value

In business terms, loss of value refers to the loss in the value of a business resulting from alleged acts of harm and negligence including, but not limited to, building damage, breach of contract, fraud, defamation, product defect and theft.Â

Small-to-medium enterprises (SMEs)

SME refers to any private business that employs between 0 and 249 employees. SMEs fall into different categories:

Micro business - A business employing fewer than 10 employees

Small business - A business employing between 10 and 49 employees

Medium business - A business employing between 50 and 249 employees

Underinsured business

Underinsured businesses are businesses that have taken out insurance policies that cover them for less than the overall value of their buildings and contents.

Sources

).

https://www.gov.uk/government/statistics/cyber-security-breaches-survey-2023/cyber-security-breaches-survey-2023

About Cameron Jaques

Cameron has worked within the SME industry for over five years, looking after all our SME commercial relations for money.co.uk including business loans, business current accounts, and business credit cards.